SVB looked well capitalised up until the depositors started asking back for their money. Their customers were startups, and thus had requirement of capital due to drying up of VC funding. This led to the bank having to find funds to settle the unexpected high with-drawl requests. As most of their funds were locked in low interest high duration govt bonds, they had to exit them before maturity by taking a loss. Leading to panic as the word got out, making their customers believe that there was a liquidity crisis in the bank.

There were several problem statements which needs to be understood in detail.

Similar customer profile

Startups were their core customer base. Similar profile customers meant they followed similar growth and problems. As the inception of the bank took place under low interest rate regime their customers had seen inflow of VC money.

Liability book strength

Pandemic added filip to this with stimulus checks and zero interest rate leading to excess liquidity in the system. Their customers were flushed with money from VCs leading to spike in the deposits.

Asset book weakness

The loan book growth of bank slowed down. This lead the bank to take decisions under wrong position sizing of assets and timing of investment.

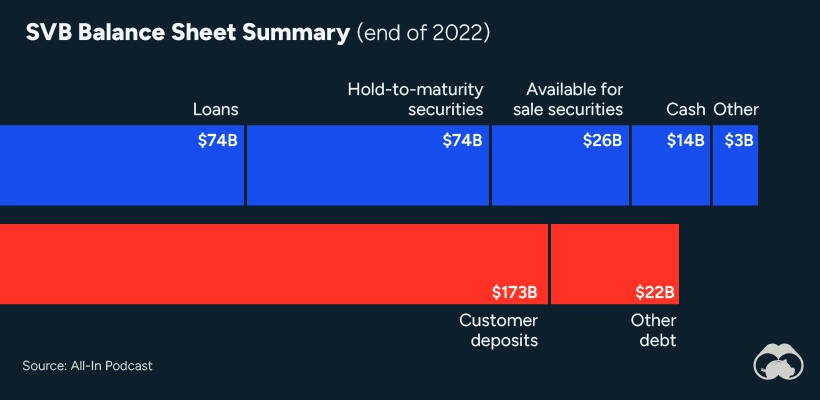

They parked $100 Billion of its funds in US Treasuries @ 1.79% with a maturity of 3-4 years in 2021. They had done so under the assumption of a slow rate hike by fed. But the quick increase lead to the safest bonds losing value.

By locking their funds at a rate of 2% for 4 years, SVB expected to get $108 on a deposit of $100 for the full term. But rates hiked to 7%, and it meant that by investing $100 at the new rate, they could get $131 over the exact same time. But this also meant that SVB would have to liquidate its old bond portfolio at a loss – when bond yields increase, their value declines, and the original bond would have declined to $77 in value.

This coincided with funding winter for startups. They could have avoided selling the bonds and hold to their full term, but customers were also withdrawing their money en masse as they had to resort to using their cash reserves.

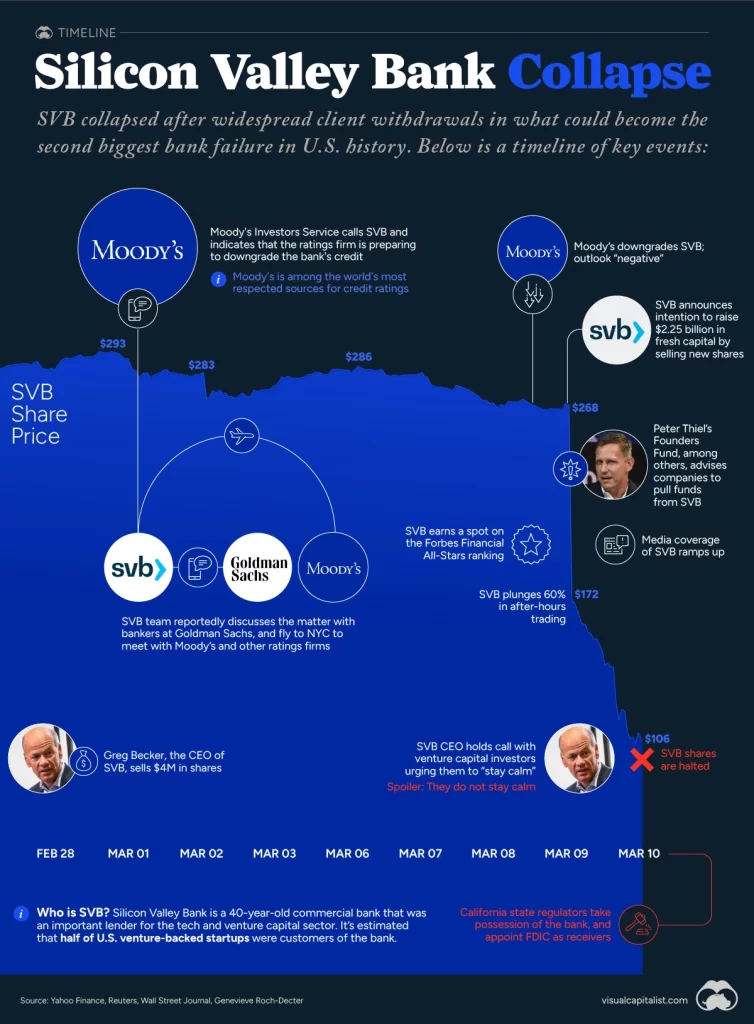

Became strap cashed for servicing withdrawals. Moody’s Investors Service threatened to downgrade their credit rating – which would scare depositors. So SVB decided to sell its bond portfolio at a loss of $1.5 Billion. The company announced on March 8 that it would be selling a third of its ownership in an effort to raise $2.25 Billion and offset the bond losses, while continuing to service withdrawals. But word got out that the bank could be facing insolvency, and when the market reopened the next day, the stock price plummeted by 60%.

All of the above dwindled their chances of raising capital.

Peter Thiel even advised companies that were part of his Founders Fund to start pulling their money from the bank.

On March 10, Silicon Valley Bank announced that they had failed to raise capital and were looking for a buyer because they had more withdrawal requests than cash on hand. Hours later, regulators stepped in and closed down the bank with the message: All of the bank’s deposits have been transferred to the new bank. Insured depositors will have access to their funds by Monday morning. Depositors with funds exceeding insurance caps will get receivership certificates for their uninsured balances.

Learning Ability to manage the Asset-Liability balance is a pertinent requirement for a bank.