Stock Volatility.. Stock has shown a deep fall since listing. Markets perception of the business was they had no clear leadership in any of their segments. Poor visibility of earnings, high ESOP cost, anchor investors exit during buyback period; has kept investors uncomfortable and wary of holding on to the business. Every upward move so far has been followed by a sell off by the previous investors like Softbank, Alibaba etc.

Thesis.. Having analysed the business I felt the current ecosystem and economics are favourable to the business. I have identified some parameters which gives me confidence on why it would be a good investment. Foremost, the stock price seems to have a margin of safety at my average acquisition cost of Rs 600.

Antithesis.. Poor corporate governance shown by the management. Keeping in mind that it is an out of favour stock; real cashflows and profitability would have to be shown for investors trust to come back. The high ESOP cost of < 4000 Cr will keep playing out on investors mind and thus the adjusted EBITDA story may be hard to sell. The longer it takes for the above to play out the effect of time on value of the investment would have to be kept in mind.

Understanding so far.. Paytm is a business with no competitive advantage. Unlike banks (also a commodity business) which has high switching cost associated with them, Paytm has no such anchor for it’s customers. Their relationship is transactional and hence retention is low. Deep pockets like Google and Amazon have already entered and taken over a massive share of the digital payments market on the consumer side. Having said that – Brand recognition, well penetrated distribution reach and strong merchant business are some of the strengths if leveraged well gives them ample opportunities of growth.

Laying down my theories in detail, the parameters which needs to be monitored and the antithesis to track…

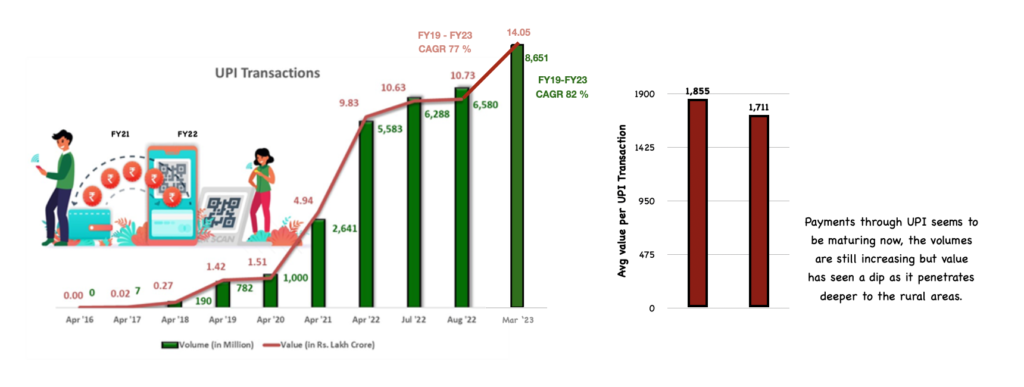

Speak about an industry with tailwinds… Payments business has the advantage of huge TAM. The infrastructure support for digital payments system given by NPCI and the governments mandate to make the UPI network free (post April 1,2022) gave a huge impetus to the penetration of digital payments in the country.

Monitor – Extent of slowdown from the volume and value growth, over the previous CAGR of 77 and 82%. If there is a significant fall in average value per transaction.

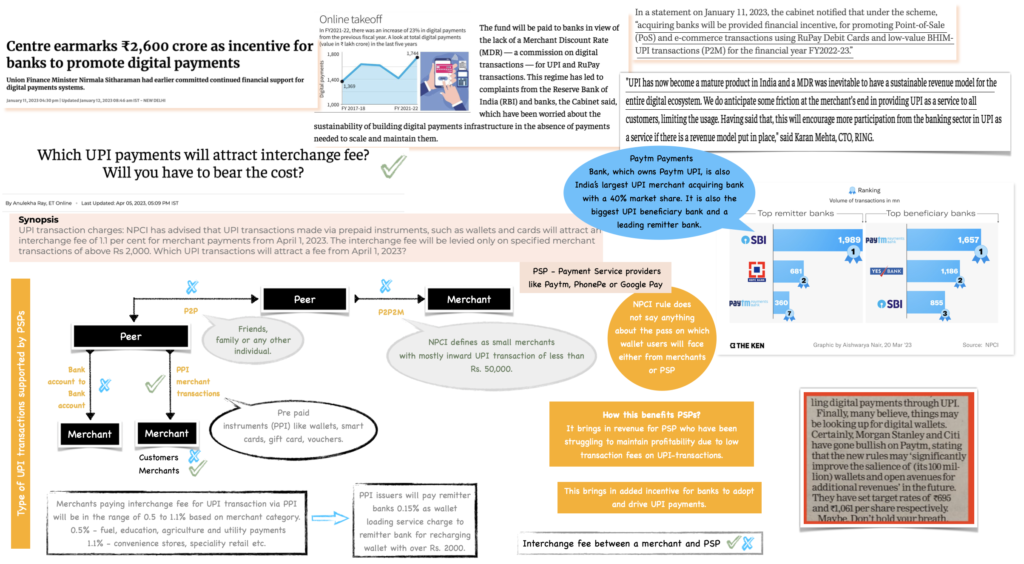

Favourable policies and Budget ear-marking.. Although UPI penetration is the backbone of growth in Payments, it has been a drag to it’s monetisation efforts after the UPI payments network became free. This was causing companies to refrain from growth and doing much innovation. Recent policy shifts and budget announcement suggests the govt is putting an effort towards the success of entire ecosystem.

Monitor -If payments over Rs. 2000 using PPI are getting charged to merchants, Track if any resistance in using UPI is observed. It should show up as a fall in average value per transaction. And what is the reimbursement being provided to Paytm by the government from the Rs.2500 Cr incentive pool.

‘The core of Paytm’s business model is to acquire consumers and merchants for payments services, and upselling them financial services, by leveraging the distribution, collections and transactional and behavioural insights. They have sharpened focus on Payments and distribution of Lending products and have prioritised these businesses in resource allocation.’

Monitor – Cross selling opportunities, newer revenue streams and their margins.

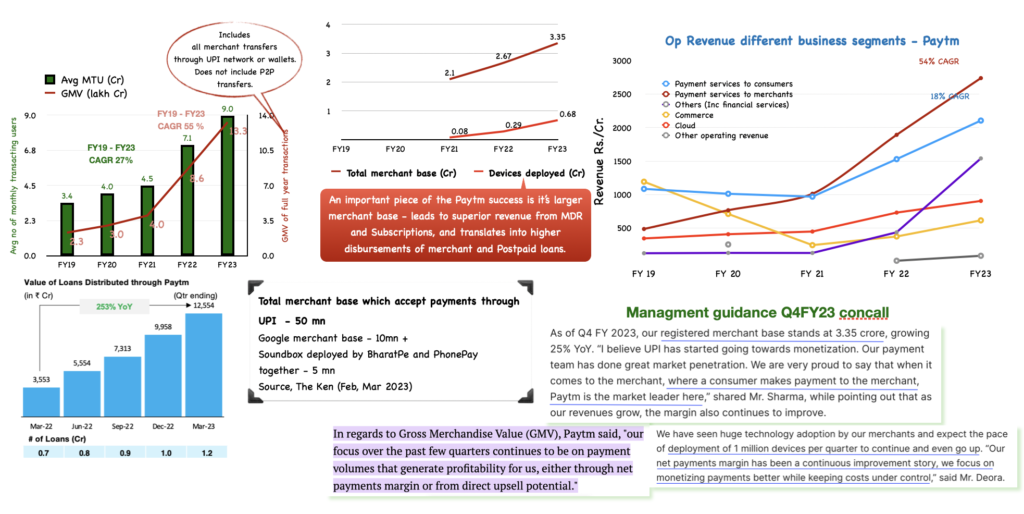

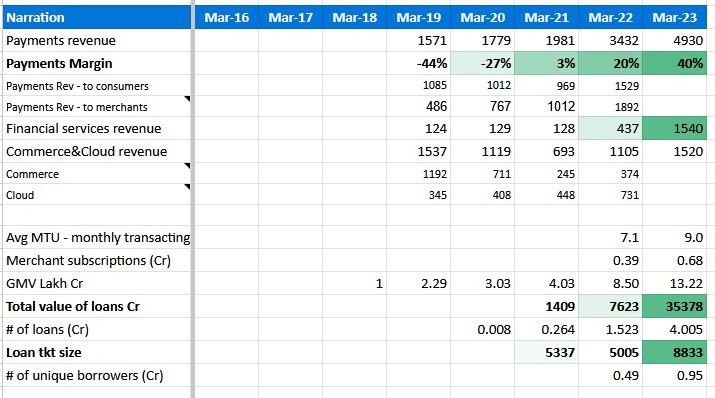

Keeping the merchants at the core of their monetisation strategy.. They focused on increasing merchants on their payments network, along with capturing a share of the UPI transactions. Value added services like the Soundbox and POS devices, helped capture this ecosystem. It helped them generate revenue by charging MDR on transaction through wallets, payment gateway fees and Subscription on devices. Their competition has realised the same and hence trying to capture a share of the merchant ecosystem. The governments is showing support by allowing MDR in PPI transactions over Rs. 2000 and reimbursement to acquirer bank for payments made through Rupay card and Bhim-UPI network. In the chart below, the growth in Gross Merchandise Value (GMV) is directly translating into merchant revenue.

Payment services to consumer revenue has also started improving by selling value added payment products like paying bills, fees, booking tickets etc; and charging convenience fees on that.

Merchant lending is another business which is showing great traction now.

Monitor – Increase in merchant base, transacting users, growth of devices and any effect GMV by allowing MDR on UPI (merchants resistance to added cost). Track the credit business by number, value of loans disbursed, provisioning for loans and NPA on books.

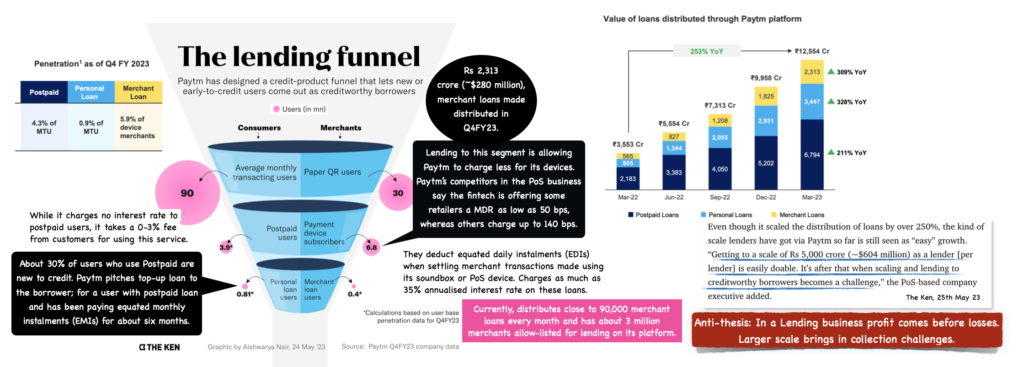

Upselling credit… Loan-distribution business became a key driver for achieving operating profitability for Paytm in H2FY23. They have started selling credit to the user base (who have been with them since past 2-3 years) and merchants on their platforms; through lending partners.

Post RBI ban on lenders to share credit risks with their partners through FLDG (First loan default guarantee), Paytm came up with an innovative proposal to keep the relationship growing. They offered forfeiture of a portion of its fee earned from loan distribution, upon failure to fulfil collection commitment. Growth in the segment shows that so far this has worked very well in their favour.

Currently they have seven lending partners, and also does collection exclusively for about 10 other lenders. Their acquired arm CreditMate helps in this collection.

Till date they have penetrated 4-6% of their active user-merchant base to distribute loans. so the headroom for growth still remains strong. Scaling up lending to credit-worthy customers beyond a point has been a challenge for all lenders, and the same risk stays for Paytm.

Monitor – Track the credit business through number of lending and collection partnerships, value of loans disbursed, provisioning for loans and NPA on books. As Paytm extends credit to the organic users and merchants on their platform coming through payments business; monitoring growth in user and merchant base is important for scaling up of the lending business. Controlled NPA now becomes the most important key to the success of this segment, as it affects their collection revenue and partner relationships.

Lending penetration to their current customer and merchant base is low, so the opportunity of growth still remains within their captive ecosystem.

How about earnings… Like all other new age companies there are some adj. EBITDA and Profit reporting which is happening. But looking at those numbers do suggest that there is an improvement in the financials.

Monitor – Instead of contribution profit, EBITDA is a better matrix to follow .

Employee and and marketing cost; as managment is indicating they will be increasing the ground staff to capture merchants in Tier 2 and 3 towns and will not shy away from any marketing push required for growth.

The utilisation of Rs. 8300 Cr which was raised in IPO.

Reason for stress in the EBITDA… High ESOP Cost is coming in the way of earnings, even though when all the other costs are going down and operating leverage is showing up.

Still trying to fully understand the effect of ESOP on shareholder’s in the long term. Currently as an employee expense it is notional and returned the non cash transaction to operating cashflow. On the balance sheet a reserve pool for it has been made, once the stocks are exercised they will be moved to Shares outstanding, causing eps dilution.

Need to figure out – Whether the ESOP was leveraged or non-leveraged? Exercise of options would be EPS dilutive; so doesn’t this show an effect on EPS before (in form of non-cash employee expense) and after (as dilution) vesting? Having returned the non cash transaction to operating cashflow at the time of recognising expense, is there an effect on cashflow at the time of exercise of options?!

Monitor – New issue of stock options. Vesting of the older options and their effect on the Cashflow.

In Q1Y24 call, managment has guided that ESOP cost will start reducing from Q2FY25 onwards.

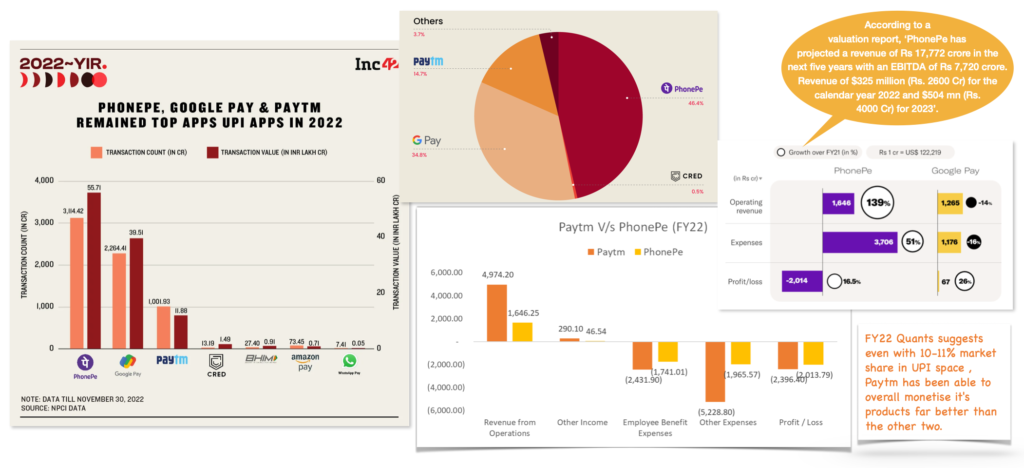

Competition.. Google pay and Phone Pe have larger share of the UPI market share by volume and value.. So when Paytm is compared to them on these parameters they do not seem to have enough strength in the business.

But upon comparing their financials it tells a different story. Revenue from operations of Paytm is more than 3x of PhonePe and 4x of Google Pay.

Google Pay is the only profitable payments company, but it has been facing issues with it’s payments infrastructure and hence losing market share.

Majority of their PhonePe revenue still comes from payments and hence overall monetisation has been poor. It also faces an NPCI dictate overhang of any one company holding more than 30/35% of UPI market share’. Herein, lies an opportunity for Paytm to increase it’s market share beyond 10-13%.. But they would compete with fintech company’s like Cred who is gaining market share in the space (even though still small) Paytm would have to move faster than them to gain market share.

Valuation.. The Rs 45,000 Cr (USD 5.6 Bn) market cap as on 13th May 2023, consists of more than Rs. 7,000 Cr (USD 0.8 Bn) in cash on their books.

Comparing it to Ashwath Damodaran’s two year old valuation; the company is showing higher growth in GMV, inline operating margins but lags on improving their take rates. Not much reinvestment has been done in the period and hence FCFF has improved. Looking at his analysis there seems to be a high margin of safety in the stock price at current levels.

Comparing with the competitor also gives the same story. PhonePe recently did a fund raise, at a valuation of USD 12 Bn (58x P/S). If compared on top-line, Paytm is available at 5.6x P/S and comes with CAGR expectation upwards of 35%, hence the stock seems cheap.

Antithesis..

Granular look at numbers… Their GMV is increasing but it’s conversion to revenue is still sub-par at 0.6%.

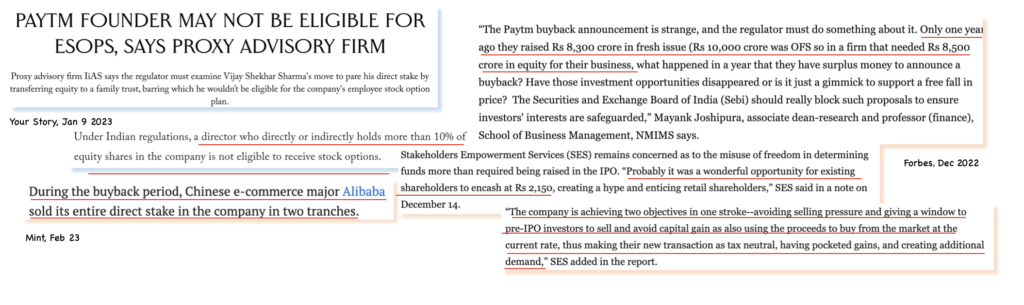

Corporate governance… Before IPO a ‘Sharma family trust’ was build and part of his ESOP was moved to that, reducing his direct stake to 9.1% from 14.7%. VSS was declassified as a promoter, but still enjoys rights of a promoter example a permanent seat on the board.

A buy-back within an year of IPO, points towards a strategy to give early investors exit.

Bought at an average price of Rs 605 in MO portfolio and SCHIL

13th July 2023

NBC and Banking Partnerships… 7 active lending partners and aim to onboard 3-4 partners in FY 2024. On 30 June 2023, announced loan distribution partnership with Shriram Finance Limited.

23rd March 2024

Thesis… was based on the multiple revenue optionality that the managment had been able to create over time for their payments business and at the same time creating opportunities that funnel growth into the financial services and lending business.

The margin of safety stock was offering at Rs. 600 seemed enough to look over the missing profitability, but the RBI regulations still made the stock correct drastically.

Reason.. the business lost a lot of revenue streams due to the ban on its payments bank.

Mistake.. in my anti thesis I had not considered the payments bank regulatory non compliance (which they had been facing for a very long time), even though a concern in managment’s corporate governance track record was noted.

Direct Impact of the RBI regulation

NPCI had allowed interchange fee for prepaid instruments like wallets and cards to acquiring banks. Paytm payments bank had been a direct beneficiary being India’s largest UPI merchant acquiring bank with 40% market share. Monetisation efforts of the UPI network was thus becoming possible. The regulation forces paytm to shut down transactions through their wallets affecting the payments revenue.

Paytm was the largest fast tag issuing bank with a decent commission income. This move wipes out that revenue stream as well.

In-direct Impact of the RBI regulation

Competition is going to take advantage of the situation leading to value migration.

- Last two months have already seen drop in their UPI volumes while that of Google pay and PhonePe improving. A regulation capping the share of these companies in UPI volumes is required to help Paytm from this loss.

- As merchants were at the core of to their monetisation strategy, thus value migration amongst them would affect them the most. Growth/de-growth in sound box has to be tracked.

As the business works as a funnel for onboarding customers and merchants through payments business and upselling financial services.

- Impact of migration on payment customers and merchants will come on the other side of business as well which is higher revenue generating.

- Growth in lending business had become the basis of Paytm investment thesis and an important factor for achieving operating profitability. But with customer and merchant growth affected their relationship with nbfc and banks should also suffer if the funnel narrows at the top..

Thus overall if the revenue gets hit the losses which the business has been making would widen further (they have indicated +Rs. 500 Cr so far). The managment would have to re-think and re-analyse the strategy overall, although I see they have been successful in the past, unable to gauge the trajectory in future.

Exited 50% of my holdings, by booking a 42% loss