Today is an attempt to understand the relationship between liquidity and interest rates – their correlation with bonds and equities, and what to expect in coming times.

I have been overly optimist about the markets since I have entered, with too much faith that in the long term the markets will only reward. But now wonder ‘How do I define long term?!’. Based on the changing macro situation, making an attempt to understand them and improve upon my risk analysis. Hoping with better understanding, fixed income will also find a position in my portfolio.

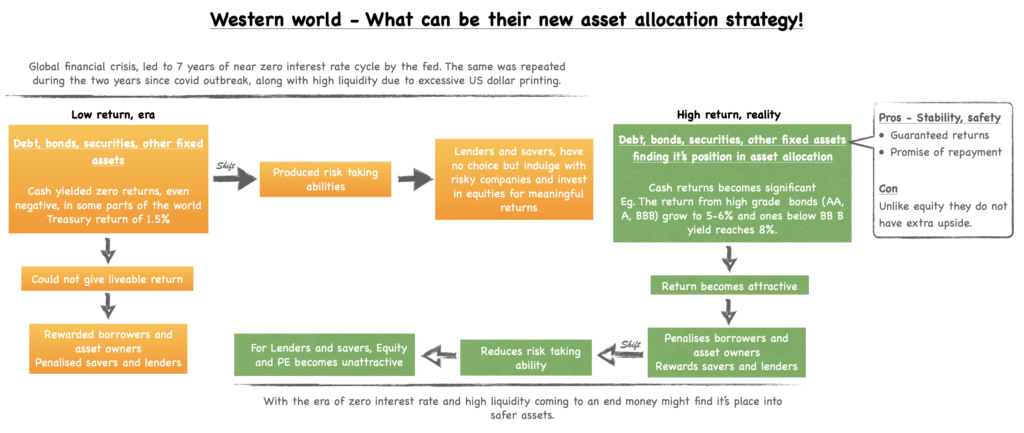

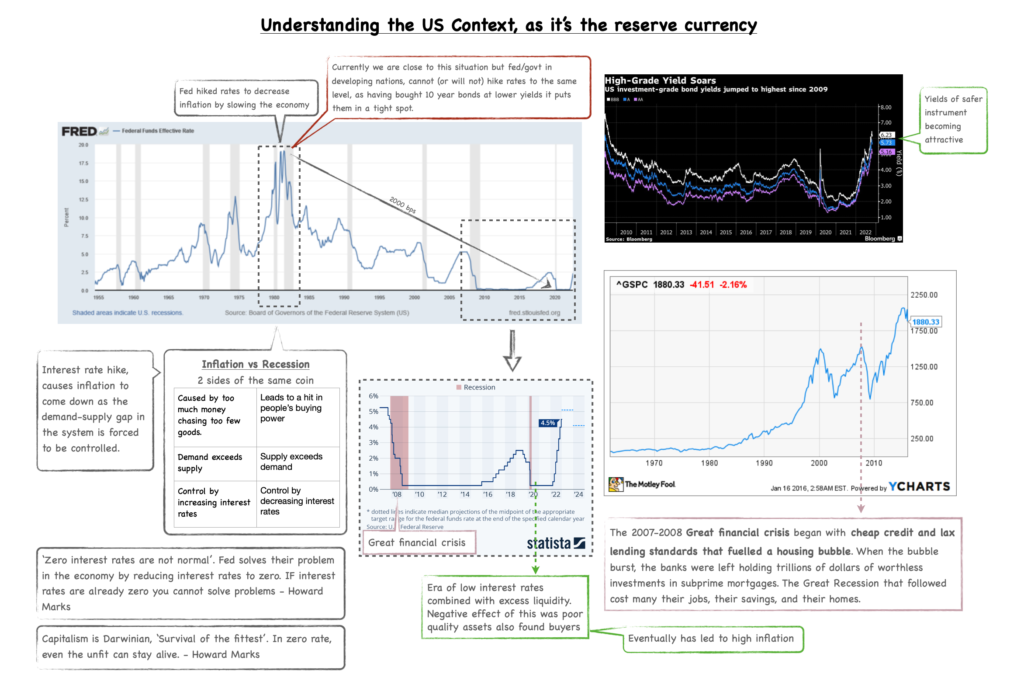

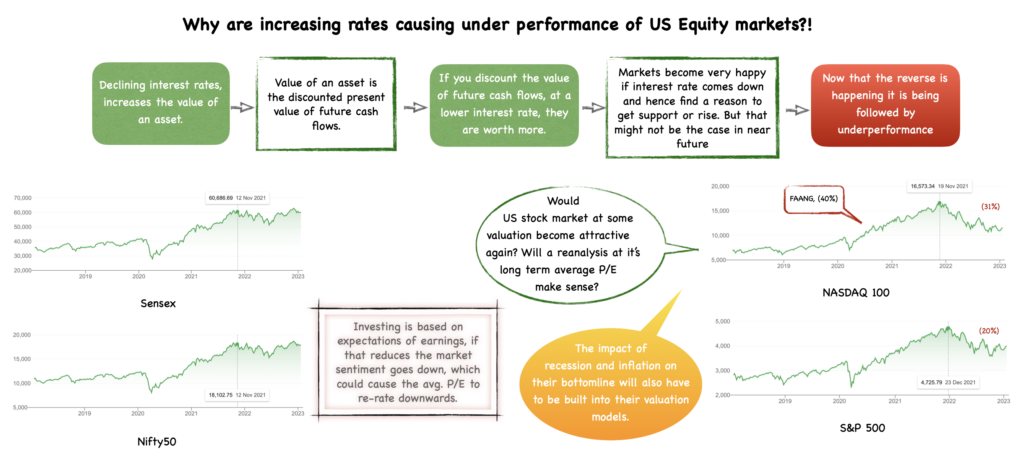

In the past two years, we have experienced a lollapalooza moment where low interest rates, combined with fed printing dollars causing excess liquidity in the system. Leading to the boom in cryptocurrency, PE and VC funding companies with just a promise of growth or a fancy idea and overvaluation of companies with stable earnings. High liquidity and low interest cost also caused a boom in housing demand and stock market went soaring. But most important observation is the fact about how they all started falling as soon as the fed announced raising interest rates.

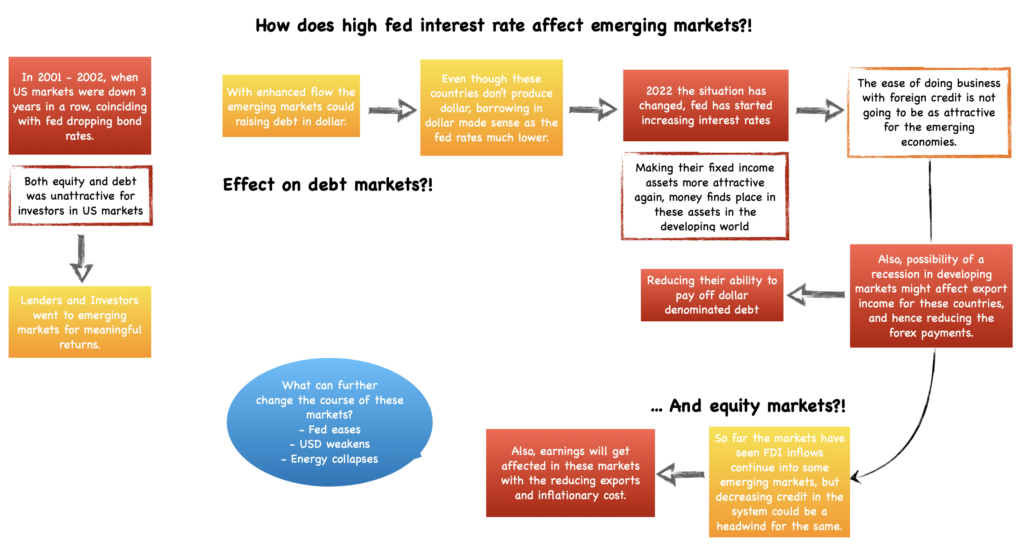

A conversation between Niraj Shah and Howard Marks (of oak tree capital) on TINA (There is no alternative) and TARA (there is an alternative) effect, has helped me get some clarity into this topic. It was more in context of the Developed economies specially USA and an impact it can have on the emerging markets.

And on the other hand there was a webinar by Ritesh Jain of Pinetree Macro, he explained the correlation of liquidity and markets, both developing and emerging.

One thing that is common in both conversations is that past 10 years the western world lived in a low inflation phase and which was a privilege, everyone started believing it to be normal. But now we will enter a ‘new normal’ which is inflationary in nature, and the world order will have to change to suit that.

‘How do one readjust, when the value of money comes down?!’

Current US Debt/GDP is 130%. According to Ritesh Jain, ’51/52 countries whose Debt/GDP crossed 130 have defaulted (restructuring, devaluation, inflation or outright default). Japan is the only country which did not default.’

Printing new dollars at this stage would only take their Debt/GDP higher. There was a discussion about printing a Trillion dollar platinum coin which is not backed by any securities like Gold or Silver, and does not affect their Debt/GDP. Although doing this is counterintuitive it could flush the world with liquidity again.

If liquidity and equity markets are coupled, we have seen a decoupling in Indian markets from rest of the world; as the NIFTY no longer mimics the fall in NASDAQ, ‘What is it that has changed?’.

It becomes important to understand and analyse, ‘How is India placed in this changing world order?’.

Some positives seem to be working in our favour at the moment

Earning outlook

- We have seen China +1 play out in certain pockets such as Electronics, specially mobile manufacturing. This gives higher optimism of getting a larger share in the current Supply chain shifts

- India Inc has shown sustained earnings uptill now, having said that last quarter a little bit of slow down was seen. Softening logistics cost will be helpful, although raw material remains a challenge for some industries.

- Banks have a clean balance sheet and credit demand surpassing deposits, and may continue if the capex cycle continues going forward.

FDI Inflows

With the above still playing out favourable for us, the emerging market funds cannot find abetter alternate for allocating their capital and hence there is money still chasing the Indian markets.

Domestic environment being supportive of growth

Better Macro

- As per Jan data by RBI, India after a long time has shown Real rate of return to be 0.5%; as the inflation has shown resilience and RBI has increased interest rates. This helps increase the value of Rupee. (Other countries with positive Real rate of return higher are Brazil, China and Mexico).

- Larger possibility of increase in Per capita income, as the economy expands.

- Revolution in payments and the digital stack will play an important role.

All this leading to more and more financialisation of income.

We have seen increasing AUM in SIP and retail participation grow from 4 mn in 2020 to 11 mn by end 2022.

As we live in a connected world now, so the fact that we can be completely anti-fragile does not bode well

- In the past one year, Foreign reserves fell by a trillion dollar. If FDI withdraws, our reserved foreign exchange goes down, the liquidity in our markets will also leave, leading to increased cost of funds for banks. If oil prices increases it can break everything for us, causing further dip in reserves and widen CAD. (All recent reports suggest energy prices are going to stay higher than the last decade.)

Domestic

- So far RBI has shown constrain in appreciating Rupee over dollar as their focus is on increasing the reserves. But if dollar depreciates even if it will be helpful for imports, our export industry will show a huge draw back.

Should also keep in mind some possible larger impacts

- When the developed world (specially Europe, large extent China) is shifting towards greener solutions. We will be taking a fair share of supply chains shifts at a cost of higher carbon emission.

- As our neighbours (Bangladesh, Srilanka and Pakistan) are showing distress in their economies, we are in a position to face heavy migration. (I am not completely sure whether it is a good or bad thing, because this helps increase our working population)

How do I translate these learnings into practice?

- Foremost would be to develop a framework for my portfolio.

- Understand the relation between cost of capital and expected ROIC, whether the growth capex in my companies still makes sense. Focus more on where the capital for that capex comes from (internal accruals or debt) and it’s impact.

- The effect of Dollar movement on the companies.

- Focus on revenue and earnings growth to keep my conviction intact in my companies, as in the current situation it might not translate into stock price movement.

- Be prepared to bare larger pains in the portfolio in mid-term.

- Clearly as fixed income is becoming attractive it is time to put an effort to understand the various options available, and be more mindful of allocation into them.

- My first long term milestone up untill now was 10 years, which coincided with the time my children would go to college. If our US portfolio takes a hit in equity growth and if higher inflation causes increased cost of University fees & living expense. A realignment in strategy is required to reach this goal.