Investment has played out differently from how I had anticipated initially. Bought at it’s absolute peak of Rs. 680 and have averaged down since then. With that the company has reached my largest investment by buying cost.

The reason I ended up buying at the peak was –

- I could not see the fall in ARV business that was showing up due to channel stocking and only focussed on the USD 1 Bn target which the managment was giving

- And again repeated the same by not anticipating the impact of one time contract in CDMO and extrapolated the revenue with the managment guidance of USD 1 bn

- When both of these normalised, huge operating deleverage started to show up because of un-utilised new and old capex

Investment thesis while adding Laurus Labs to the portfolio..

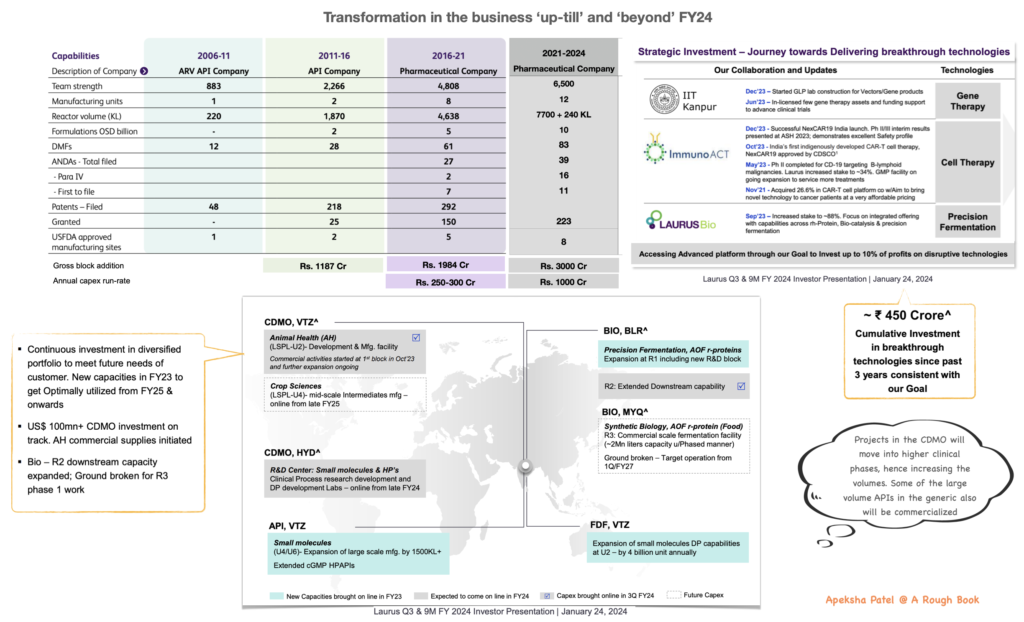

In FY21, the company experienced significant growth, supported by its gross block expansion from Rs 1100 Cr to Rs 3000 Cr over five years. Leading to a revenue increase from Rs 2832 Cr to Rs 4814 Cr, with a 22% CAGR between FY16 and FY21, while achieving a ROCE of 41%. They evolved from an API to a pharmaceutical company.

Future guidance also sounded very promising with a sales target of USD 1 Bn by FY23, and the capex plans indicated that the transformational growth would continue.

Taking a hindsight view - mistake made while forming thesis..

Invested at peak ROCE and peak margins, no margin of safety left as excessive optimism was already priced in. My thesis relied on future capex driving growth, but I failed to anticipate that the capex incurred before becoming operational would impact the ROCE negatively.. Additionally, the custom synthesis PO was lumpy in nature (they were reaching 30 % contribution from synthesis business much more earlier then guided) and that was leading to peak EBITDA margins of 32%.

Why have I continued buying?..

Since FY21 they have worked towards metamorphosing into a Lifescience company..

- Richcore acquisition was a stepping stone into capturing the biotechnology opportunity. Their current focus would be in large scale r-protein fermentation focusing in food industry.

- Within custom synthesis added Crop sciences and Animal pharma clients, and developing a dedicated block for the same.

- Collaboration with Immunoact and IIT Kanpur for cutting edge technologies in cell (like Car T) and gene therapy.

As the haze in revenue have cleared out (post ARV de-growth stabilising and the one time gain from custom synthesis purchase order normalising), operating deleverage is coming through. FY24E revenue is largely similar to FY21, with profitability fallen to 20% of FY 21 earnings; as a lot of operational inefficiencies are currently present with the gross block doubling and team strength having increased by 35%.

Expected result of this transformation

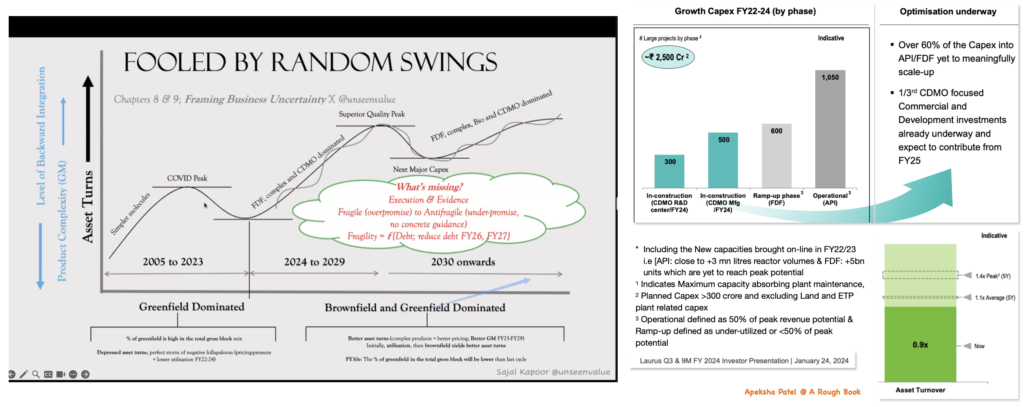

The effect of Laurus transformation was best described by Mr Sajal Kapoor in his recent webinar on ‘Anti Fragile Businesses’. Currently optimisation of FY22-24 capex is underway, which would result into better asset turns, probably surpassing the previous high of 1.4x. This would come as they shift from simple to more complex molecules along with higher gross margin CDMO business, and as the capex shifts from greenfield to mix of greenfield and brownfield.

Keeping in mind managment’s missed guidance of USD 1 Bn and debt in the business as negatives, key reasons for staying invested and believing for a turn around –

- Proper utilisation of capex and resources, brings in a possibility of high operating leverage showing up

- The shift from an ARV company towards life sciences, brings in a lot of optionallities in the business

- Managment’s past execution track record has been good

- It is nearing a point where reversion to mean should be expected

Investment is currently at 9% by buying allocation and 3.5% of total portfolio value @ an average price of Rs. 508

16/09/25

Sense Check on Valuation @ stock price of Rs. 900 (EV of Rs. 50,920 Cr)

@Stock price of Rs. 900 (EV of Rs. 50,920 Cr)

Running a valuation analysis, expecting top-line growth to be the same in both scenarios and EBITDA margin of 30% (as guided); but with difference in incremental revenue mix shift towards CDMO. This results into difference in contribution of CDMO to EBITDA. Hence the final valuation the business gets. This will come from FY26 gross block of Rs. 7200 Cr.

Fy28E Rs/CR | 40% CDMO – contribute 60% to EBITDA | 50% CDMO – contribute 65% to EBITDA |

Revenue | 9000 | 9000 |

EBITDA @ 30% | 2700 | 2700 |

EBITDA CDMO 45% margin | 1600 | 1800 |

EBITDA non CDMO | 1100 | 900 |

EV/EBITDA CDMO 25x | 40000 | 45000 |

EV/EBITDA CDMO 9x | 9900 | 8100 |

EV | 49900 | 53100 |

Less: Net Debt | 2964 | 2964 |

Add: Cash | 144 | 144 |

Implied equity value | 47080 | 50,280 |

No of shares outstanding | 53.68 | 53.68 |

Stock price | 877 | 936 |

Going by the above analysis, 3 years growth is already in the price with considered CDMO and rest of the business EV/EBITDA at 25x and 9x resp.

Even if we consider Laurus’s business to be inferior than Divis; if the business is able to achieve our assumptions, a re-rating of the 18x-20x (blended) EV/EBITDA can be expected over the next 3 years.

A 25x or 30x multiple leads to EV (3yr CAGR) of Rs. 67500 Cr (11%) or Rs. 81000 Cr (17.5%) resp.

Divi’s Laboratories with 50% of CDMO revenue, has traded at an avg 40x and 30x EV/EBITDA multiple over 5 yr and 10yr resp.

Cash valuation comparison – Expect the business to do Rs. 1000 Cr operating cash in FY26 and reach Rs. 1500 Cr by FY28, bringing the FY26 and FY28E EV/OCF to 50x and 33x resp. Even if Laurus does not get a re-rating to it’s current cash multiple, based on growth expectation an EV of Rs. 75000 Cr can be reached. This in line with the EV expectation if EV/EBITDA multiple gets a 25-30x multiple.

Rs.1800 Cr is the average CFO generated by Divis in past 5 years, currently trades at a multiple of close to 95x.

3 years growth of EBITDA and cash may already be discounted in the current stock price. But if the business performance is as expected, a stock re-rating leads to a 14-17% stock CAGR over next 3 years.

Investment is currently at 6% by buying allocation and 10% of total portfolio value @ an average price of Rs. 528

16/09/25

Laurus bio and it’s role in next phase of growth

@ Stock price of Rs. 975 (EV of Rs. 54,800 Cr)

At the time of acquisition, Richcore was a research-driven biology company having large scale fermentation and capability in animal origin free recombinant products…

Full scale, fully integrated biotech company — makes ingredients for cell culture (high gross margin business but low opportunity), enzymes (for health, nutrition and industrial, TAM is larger, where scale and cost remains important) and had limited recombinant engineering capability. CDMO optionality is where the company saw growth from there-on (two contracts were already signed).

Now, Laurus Bio offers microbial precision fermentation product development and manufacturing expertise as a service (CDMO), along with recombinant DNA engineering to bio-manufacturers — clone development, strain engineering, bio-process development and scale-up to large-scale commercial manufacturing.

Then: Mass produce molecules (precision fermentation), particularly animal-origin-free recombinant proteins.

Now: They can reprogram a friendly microbe with a new gene (recombinant DNA) and grow it in tanks to mass-produce useful molecules (precision fermentation), offering end-to-end CDMO from clone/strain to GMP supply.

Global Precision fermentation (products made via engineered microbes) market size was estimated at USD 4.01 bn in 2024 and is projected to reach USD 34.61 bn by 2030, growing at a CAGR of 43.5% from 2025 to 2030.

Growth plans

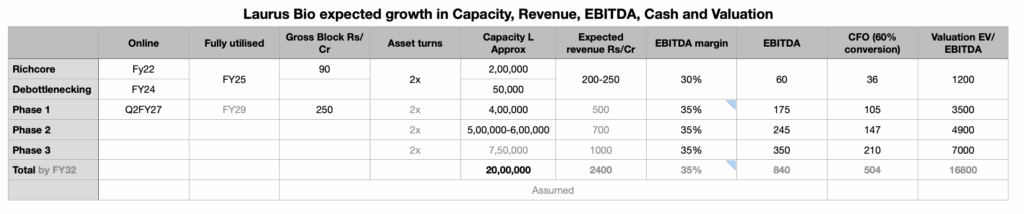

- FY21, 72.55% stake in Richcore was acquired for Rs. 247 Cr (valued equity of Rs.340 Cr); it had a total fermentation capacity of 10,750 L (2 reactors of 5,000 L & 3 reactors of 250 L each). Second manufacturing plant near Bengaluru was expected to be completed by end of March 2021. Expected annualised Rs. 60 Cr revenue (equally split between; ingredients, enzymes and CDMO), Rs .24, 25 crores EBITDA for full year. Bringing the valuation to 14x EBITDA. Guided to be 70% gross margins business. R1 gross block was Rs. 38 Cr.

- FY22, Laurus Bio R2, 4 x 45,000 L reactors came online. Laurus did not put fresh capital in the asset. Part of the capital expenditure is funded by the customer for the new plant. R1+ R2 combined gross block close to Rs.90 Cr.

- FY24 de-bottlenecking was completed at R2 (by purchasing a small patch of land adjacent to R2), adding 20% more capacity.

- Ph 1 capex started at Vizag (Shifted from Mysore R3, for fast tracking) will add 400,000 L by end of FY26. With a capital outlay of Rs. 250 Cr

- Plan to add another 500,000 – 600,000 L in Ph 2.

- Reach a total of 2 mn L by end of Ph 3. Not sure if any of the the 2mn L would be converted into a GMP facility, but the company aspires to enter the therapeutic proteins sometime in future.

Gross block of Rs. 90 Cr + de-bottlenecking capex (total capacity of 2,52,000 L), has the ability to reach Rs. 200 – 250 Cr revenue on steady state (approx. 2x asset turns) @ 70% gross margins.

My assumption is Laurus Bio currently generates Rs. 35 Cr cash from operations, which would reach Rs. 100 Cr by FY29 and scale-up to Rs. 500 Cr by FY32. Which brings it to a CAGR of 45% between FY25 to FY32; in-line with the industry growth.

Amount of investment required for any non-therapeutic fermenter, whether using for ingredients or enzymes or CDMO, will be similar cost. Therapeutic proteins, would require additional investment into GMP environment like quality control and other parameters

Out of the current gross block of Rs. 6250 Cr, Laurus Bio is not more than Rs. 120 Cr. The Rs. 9000 Cr revenue in FY28, no contribution from Laurus Bio has been considered (thus no consideration in valuation).

Expect mix of Laurus Bio in the overall revenue to start increasing from FY28 onwards. Currently at 3% of the overall revenue should double to 6% by FY28, while their contribution to EBITDA remaining higher than that. FY32 is when it would start contributing meaningfully to the overall business, expecting it’s share in top-line to reach 14 -15%.

This business line should support in the overall business re-rating to > 20x EV/EBITDA.

Investment is currently at 6% by buying allocation and 10% of total portfolio value @ an average price of Rs. 528