Invested since 2015, at an average buying price of Rs. 588 (adjusted for splits and preferred share issue in 2020).

Compound Annual Growth Rate (CAGR) of 22% in 8 years, excluding the consideration of the de-merged Jio Financial Services (JFS).

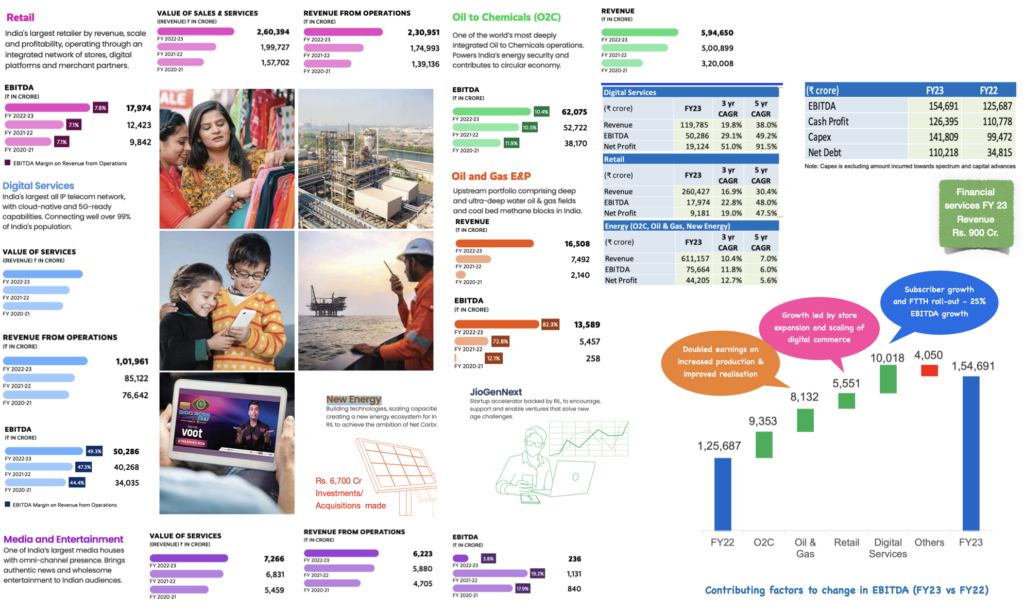

During this timeframe, the company has transitioned its focus from petrochemicals and refining, into retail and telecom/digital sectors considerably.

The question is about opportunity cost. It is currently the highest position in my portfolio at 12% (+1% JFS), so would holding a large position in it still make sense? Or some profit booking should be done?!

My primary understanding right now is separate listing of it’s different business units, would have value unlocked.

The individual segments could attract more focused investor interest, allowing them to be valued based on their specific growth prospects and financial performance. Additionally, the listing of each business unit can enhance transparency and provide investors with a clearer understanding of the individual operations and financials. This increased transparency may attract a broader investor base, potentially leading to improved liquidity and valuation multiples for each listed entity. Also, giving the optionality to exit the businesses which does not fit into my portfolio construct.

Evaluating each business-unit, in-order to understand the actual value of entire business. At this stage not making consideration of the holding company discount it might be carrying.

Sum of total part valuation (SOTP) of the business

The fund raise done by the company in recent past gives us a good estimate of value for it’s different business segments.

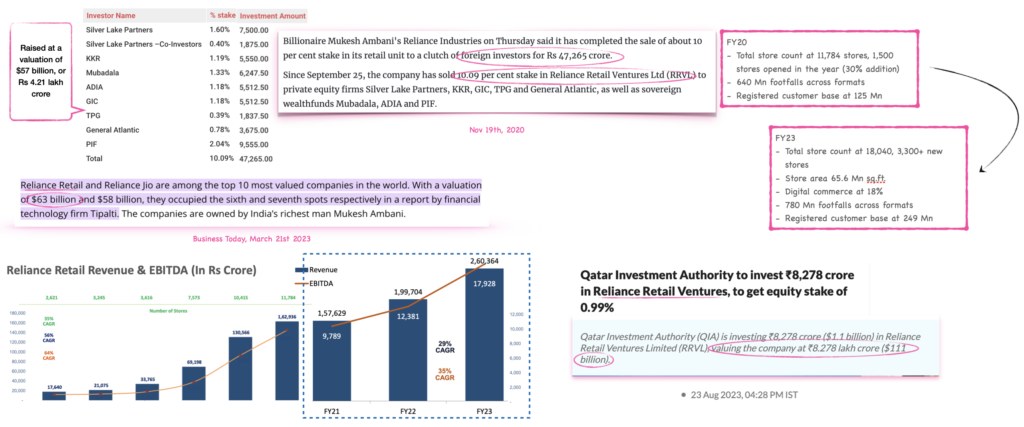

In Aug 2023, Reliance Retail Ventures Ltd., raised funds at Rs. 8.2 lakh Cr (USD 111 Bn) valuation, which is double the value they got in 2020. Giving them a 3.2x Price to sales, as compared to the earlier value of 2.6x. Considering the business has continued to grow at 30% CAGR in the past three years, and EBITDA CAGR surpassing that growth suggests efficiency is improving in the business. Also, revenue growth has surpassed the number of stores added, reflecting improving unit economics per store.

Based on the above, let’s conservatively assume current Jio platform valuations at USD 90 bn (Rs. 6.6 lakh Cr).

Now making the SOTP based valuation done by Jeffries as the basis to understand the right value for Reliance Industries.

This analysis was conducted prior to the demerger of the company’s financial business, Jio Financial Services (JFS). It’s important to note that the Sum of the Parts (SOTP) based valuation indicates a potential value upside of approximately 33% from the stock price of Rs. 2331. However, this assessment appears to be rather conservative.

In this valuation framework, the retail segment falls just short of Qatar Investments’ Rs. 8.2 lakh crore investment in RRVLs’ recent funding round. Likewise, Jio Platforms’ Rs. 4.4 lakh crore valuation matches the 2020 investor funding. Given subsequent business growth, the SOTP valuation appears low.

Furthermore, it’s noteworthy that JFS was listed with a market capitalization of Rs. 1.45 lakh crore (with a higher value compared to the considered Rs. 1.2 lakh crore), hence being value accretive for it’s shareholders..

RIL market cap post price discovery of it’s financial arm remained at Rs. 17.5 lakh cr, leading to a value unlock of Rs. 1.45 lakh Cr fot it’s shareholders, in form of JFS business. SOTP shows, Retail and Jio alone hold Rs. 14-15 lakh Cr in market cap, leaving a similar upside for rest of the business.

All-in-all, The elephant can still dance… Evaluating each business-unit, in-order to understand the actual value of entire business. At this stage not making consideration of the holding company discount it might be carrying.

Reliance industries before and after demerger of financial business

As on 30th March 2023

RIL Market cap – Rs. 15,77,093 Cr (USD 191 Bn)

RIL Net worth – Rs. 6,68,880 Cr (USD 81Bn)

RIL Revenue – Rs. 9,74,864 Cr (USD 118 Bn)

RIL Profit – Rs. 73,670 Cr (USD 9 Bn)

RIL EPS – Rs. 98.0 (USD 1.2)

RIL share capital – Rs. 6766 Cr (USD 0.8 Bn)

As on 30th March 2024

RIL Market cap – Rs. 20,14,011 Cr (USD 241.5 Bn)

RIL Net worth – Rs. 7,42,922 Cr (USD 89.1Bn)

RIL Revenue – Rs. 10,00,122 Cr (USD 119.9 Bn)

RIL Profit – Rs. 79,020 Cr (USD 9.5 Bn)

RIL EPS – Rs. 102.9

RIL share capital – Rs. 6766 Cr (USD 0.8 Bn)

Update in Jio Platform valuation - 19/03/24

Jefferies has valued Jio Platforms at 11.1 L Cr, in anticipation of an IPO. This is rumoured to be in the radar in-order to provide an exit for PE firms that entered in 2020 (and own roughly 33% of the business) at an average valuation of 4.5 to 4.8 lakh Cr.

Re-look at the Valuations - 12/03/25

Market Cap – Rs. 17,00,950 Cr (sans Rs. 1,43,000 Cr JFS)

Ambit has downgraded the Reliance Retail Venture Ltd (as it move towards IPO) to USD 50 bn (ie P/S of 1.3x). This is much below the valuation at which it raised funds 2 years back at a valuation of USD 104 Bn (P/S of 2.6x). The reason is the moderation in growth.

Cost cutting measures, slowdown in store expansion and integration of reliance brands is seen as a way the company is trying to increase it’s IPO valuation. Thus, they have been able to expand their operating margins to 8.6%.

As much of RRVL’s growth also is in-organic, the total capital employed and the efficiency/returns of that needs to be figured out; in order to determine what multiple it deserves.

Jio Platforms USD 110 Bn valuation was based on the BofA report of 2020 and 2024. The company has achieved 482 mn subscribers (against estimated 538 mn) with an ARPU of Rs. 203 (estimated Rs. 200) and reached an EBITDA margin of 53.9% (estimated 50%); for the quarter ended in Dec 2024. While it is trailing behind in terms of number of subscribers have achieved unit economics, reflecting in better profitability.

When compared to Airtel’s market cap of Rs. 9,85,000 Cr (USD 111 Bn) this estimation is slightly higher (as Airtel has higher EBITDA and better ARPU) but not very far fetched.

My holding in Reliance (RIL and JFS combined) is still giving a >18% CAGR return .