@ Current market of Rs. 1,02,000 Cr Based on some basic analysis looking at the growth in topline numbers, and considering the standalone business turned PAT and OCF positive, built a tracking position in the business.

Bought in Oct ’23 @ avg price of Rs. 119, 1.3% of portfolio

Analysing the standalone business

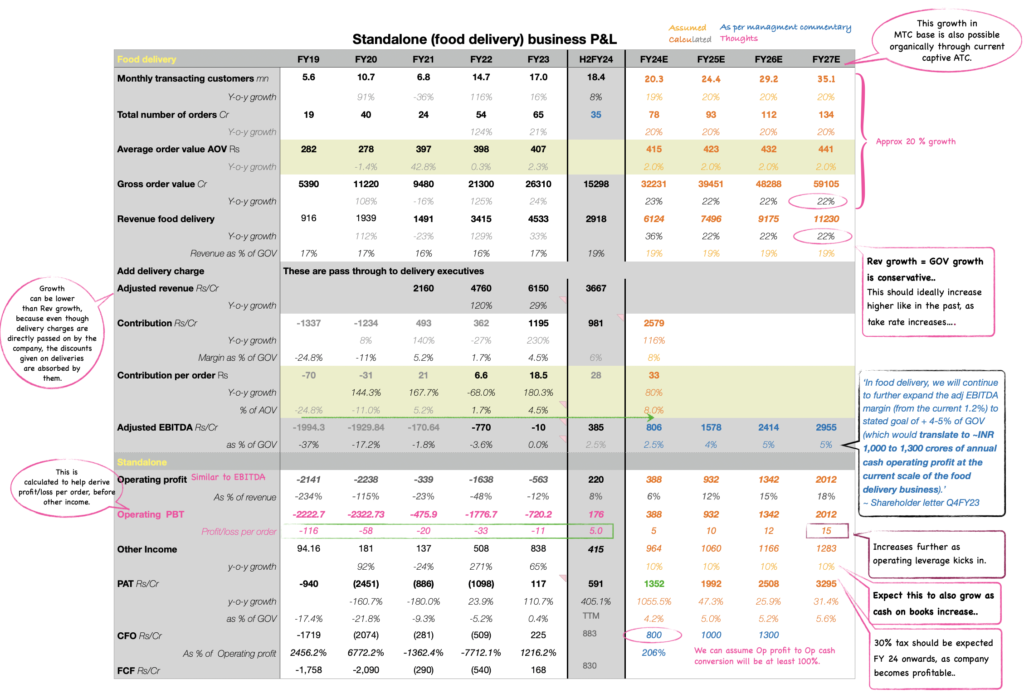

@ Current market of Rs. 1,18,000 Cr Standalone business turned positive at PAT and OCF level in Sep 22, and with sustained profitability in subsequent two quarters has resulted in the stock bottoming out at around Rs. 50 in March 23. Creating my screen shot of growth expectation for the Standalone (food delivery segment as it contributes > 95% of revenue) business in order to understand the present valuations, and set return expectations.

There are many factors suggesting sustenance and improvement of profitability in the medium to long term..

- Business is expected to continue with Gross Order Value (GOV) growth of greater than 20% over next 5 years. This can be expected with no of orders (volume) growth and AOV (value) growth.Total no of orders will grow as Annual transacting customers (ATC) order more frequently monthly; currently no of monthly transacting customers (MTC) are 1.8 Cr ie 30% of ATC (6 Cr). Growth would also come with increase in frequency of ordering by these customers, plus with new customers getting added. While increased penetration would come from macros like changing food habits and increase in per capita income.

AOV growth coming with increase in order size, adjusting for hike in food prices taken by restaurants and increase in delivery charges by the platform.

- As the business mature Take rates (% of GOV which the business keeps for itself) increases, thus increasing the Revenue of the business. It comes from two components and the optionalities for which should also improve as the business matures.

Restaurant – They already earn a good commission from the business and up until now it has been the primary source of revenue for the business.

Delivery platform – For the first time introduced delivery charges of Rs. 2 in Aug and hence delivery also started contributing to the take rate. The platform is also adopting dynamic platform usage fees on days of higher demand (like we saw on 2024 new years eve).

Advertisement income – Has 90-95% margin is 3-3.5% of GOV currently, any increase flows directly into the bottomline.

- Improvement in per order economics. Contribution per order has turned positive now and should increase further as take rates grow, while at the same time promotions and discounts for client acquisition reduces. Operating earnings per order has reached Rs. 5 per order, expect it reach Rs. 10 in coming quarter and improve further from there on as operating leverage shows up in fixed costs.

- Operating cash generation should be expected higher or in line with PBT, as the company has -ve working capital cycle and ESOP expense will also get added back. Sustained FCF growth as future reinvestment in the vertical would be limited.

- ROCE improvement from here on, as the business would not have a requirement to raise capital through equity (other than the stock option dilution) or debt and returns are expected to be good. Expect it to be a high ROCE business upon maturity.-

And that business will remain part of a duopoly..

With network effect and immense customer habit data, even a deep pocketed new player will find it difficult to sustain. Already saw that in case of Uber eats and Amazon.

With high terminal growth ..

As market penetration is low currently. Frequency of ordering and average order value is expected to grow as per capita income increases. Thus it bodes very well with the India growth story and the changing habits which comes along with that.

How much should be my return expectations based on current valuations?!

As the stock trades at a market cap fo Rs. 1,17,000 Cr, 160% above the price it bottomed out, it is important to understand how much future growth is already factored into the price.

The ESOP cost taken is in the standalone business which is already turning positive at PAT level without making any adjustments.

Leading to which the business has shown profitability at consolidated PAT level in last two quarters. If Blinkit also break’s even by Q1FY25 based on managment’s commentary, the drag on consolidated PAT will also stop.. Hence we can assume the standalone PE as consolidated PE and give 1x P/E to Blinkit business, and assume the full valuation is adjusted for the food delivery business for now…

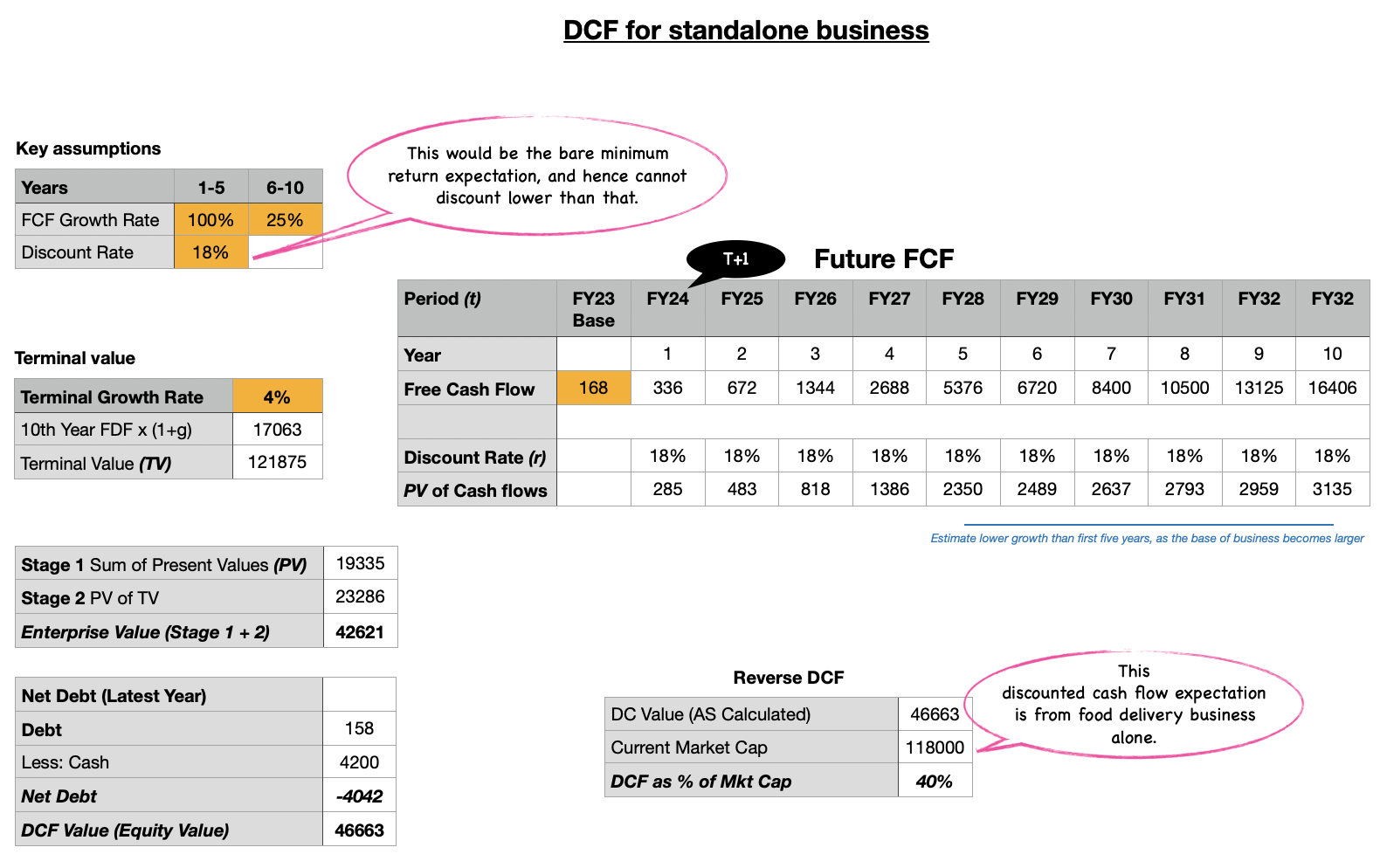

With visibility of profitability and FCF generation in the food delivery business over medium to long term, a DCF could give us a good picture of how much discounting of cashflows is already done at it’s current market cap..

Even at a minimal discount rate of 18%; the current price factors in more than 80% CAGR in FCF for food delivery business over next 10 years and a terminal growth rate of 4%. With those assumptions the current discounted value of future cash flows from standalone business remains just 40% of total market cap @ Rs. 1,17,000 Cr.

For my investment to stay secure or bore returns 18% or higher..

- FCF growth in Year 6-10 must increase above the expected 25%

- Blinkit contribution to profitability and FCF would be required.

So investing at this stage I see a medium term risk if the managment guidance of ‘Rs. 1000 to 1300 Cr OCF and Blinkit break even, do not come through’.

Stock has no margin of safety, but as there is momentum in price (which is expected to sustain as the operating leverage shows up and there is visibility of PAT and FCF growth), I will hold on to the 50% position I have built and double up if I get it at a 20% discount from my current buy .

I will book profits or exit if the cash generation is not higher than my analysis at consolidated over next 6 quarters. My actual return expectation will reamin higher than the 18% discount taken.

Jan ’24 doubled the quantity @ avg price of Rs. 139, taking it to 3.3 % of portfolio

Food delivery (Standalone) business performance already priced into the valuation. What growth expectation from Blinkit already factored in, and can it be sustained?- 14/06/24

@ Current market of Rs. 1,64,004 Cr

Food delivery business has shown a sharp growth in FCF, reaching Rs.1342 Cr (standalone) in FY24. This is two years earlier than my DCF expectation of FY26. Almost 3.5 years earlier than the estimate done in the DCF by Ashwath Damodaran (done at the time of IPO).

Reason being Adj EBITDA in past quarter reached 3.3% of GOV, bringing it to 2.9% annually, which was higher than my 2.5% estimate.

Managment has been guiding for 20%+ GOV growth and GOV to reach 5% of adj EBITDA. In the last quarter, the 28% YoY GOV growth was driven by 5% YoY AOV growth and 23% YoY Order growth. And the 23% YoY Order growth was a result of 14% YoY growth in avg MTC and 7% YoY growth in avg monthly order frequency.

The high cash on books leads to high other income, it thus cancels out the ESOP cost. Hence the food business must continue to grow FCF in line with it’s PAT.

Thus looking at the healthy volume and value growth, healthy conversion to cash and the probability of continuity of similar growth, there is optimism of the food delivery business profitability and cash generation from here on.

But the current valuation factors in much more than the good visibility of cashflows from Food delivery business.

Outline of guidance and commentary is as under

- ‘GOV to continue growth at 60%+ in medium term.’ Shown a 93% increase in GOV, reaching Rs.12469 Cr in FY24.

- ‘Aiming to get to 1,000 stores by the end of FY25,’ thus adding 475 new stores (currently 526, they were 377 in FY23). ‘70% of blink it stores were profitable’ in Q3Fy24 (ie 368 stores).

- ‘Break even in contribution for new stores is happening in 2 months. But from break even to 5% contribution cannot be predicted at this point in time.’

- ‘With this aggressive store expansion planned (almost 2x store count in 12 months), the overall adj EBITDA in business is likely to hover around zero for the next few quarters. In steady state, guided for a 4-5% Adjusted EBITDA margin (as a % of GOV).’

- ‘Per store throughput expect to not go down with expansion, although it can be lumpy, but over quarters it will smoothen out.’

- ‘Top 8 cities contribute 90%, and still remain under indexed in them. Focus of next few quarters is to bring Bengaluru, Mumbai and Hyderabad to the penetration of Delhi NCR, both in terms of store footprint and GOV.’

Impact of aggresive expansion plan

- Avg. throughput per store gets affected, as the number of matured to immatured stores becomes equal.

- Change in focus to geographies like Bangalore and Mumbai, where competition Swiggy Instamart and Zepto has a better foot hold because it is their home market. Breakeven may take longer.

- As the larger players like reliance retail, amazon and big basket enter the market, would come with a cash burn strategy. Thus if push comes to shove, Blinkit might be forced to follow suit. They are currently showing pricing power by charging Rs. 20 per order but because the business has no real moat (unlike food delivery) it might not sustain. This would show downward movement in unit economics and thus leading to operating deleverage.

As adj EBITDA stays zero, thus bringing down the consolidated profitability and cash generation.

Aggression for growth will come with delayed cash and profit.

Instead of waiting for a 20% discount (from Rs. 139) to buy the stock, I have added at 33% higher cost. This is with keeping in mind that the Blinkit expansion may bring in pressure on consolidated level for next year.

The Rs.12,241 Cr (March FY24) in closing cash on the books, brings in balance sheet strength, would be the arsenal to support the Blinkit expansion and future M&A for growth opportunities. Visibility of < 40% topline growth and achievement of steady state FCF generation from food delivery business, was the thesis behind adding at this price.

Added @ avg price of Rs. 185, taking it to 3.4 % of portfolio

Is Blinkit resilient Amid Hyper-Growth and Rising Competition?- 17/03/25

@ Current market of Rs. 1,96,752 Cr

>Blinkit contribution margin reached 3% even despite rapid expansion. 1,000 orders per day is the point where typically a store becomes contribution positive, which comes in around 2-3 months for a new store. As for new store additions, at an aggregate group level that timeline hasn’t changed. ~Q3FY25

While increasing number of orders and AOV is the key to make the business model successful, and for which they have been continuously increasing the SKU and growing their network. Initiatives taken are in-line to improve the same..

Increase in share of non food category.. Managing the SKU well has had a positive impact on Blink-it increased AOV, leading to improving contribution margin. Revenue mix has has shifted to 60% food and 40% non-food.

Bistro..

Private label

Zepto has already done the same. They directly compete with the FMCG companies by launching their own pvt label, with the advantage of pushing their own products on the platform.

Blinkit’s Take rates (the percentage of GMV it retains as revenue), the major contributing factors are

Merchant commissions.. Charged to partner stores (kiranas, supermarkets, dark stores, pharmacies, etc.) on each order.

Varies based on product category:

High-margin products (beauty, electronics, gourmet foods) → Higher take rates (~15-25%)

Low-margin staples (fruits, vegetables, dairy) → Lower take rates (~5-10%)

Advertising and Platform fees

Brands pay promotional fees to get priority placement in search results or home screens.

Stores may pay listing fees or higher commissions for better visibility.

FMCG brands like Nestlé, HUL, and PepsiCo use Blinkit for new product launches, boosting take rates.

‘Social Ads’ is Zomato’s Ad tech platform, how well they monetise this is going to be key for future success..

This leverages Zomato’s data driven targeted ad solutions to get the most of digital marketing spends for brands and restaurants. It’s a DIY tool which allows brands to run campaigns on-platform and off-platform. For off-platform, Zomato has tied up with Meta. The ROI which they are able to generate by running targeted Ads for these campaigns, would be instrumental in creating an asset light revenue stream.

BofA estimates Quick commerce ad revenues to be around 3-3.5% of GMV. And expect it to improve to 5-5.5% in coming years for select platforms. Etsy, Amazon and Nykaa register 5.7, 5.5 and 5.4 ad revenue as % of GMV resp. This is a 90% EBITDA Margin business.

Zepto revenue from Ads has crossed Rs. 1000 Cr on an annualised basis which is in line to u3-3.5% for , don’t have the exact number for Blinkit yet.

Cash Position (+ve as they have cash for Blink-it growth, -ve as draining cash from food delivery which is also not enough and Equity dilution has been taken)

Standalone business ie food delivery has started making > Rs. 1500 Cr in FCF..

But consolidated business would require re-investment of that cash along with capital raise to support Blink-it growth. Equity has also been diluted by doing a QIP in Nov 25. Raised ₹8,500 Cr via QIP at ₹252.62 per share to bulk up cash reserves; post this Cash balance increased to INR 19,235 Cr.

Zomato food delivery business has not shown growth in MTU past few quarters and may struggle to reach the previously estimated 24.4 mn customers by FY25. The GOV growth in past quarter has also shown slow down, but that cannot be the benchmark and should be monitored. I am getting a bit pessimistic of 20% growth in MTU from here on.