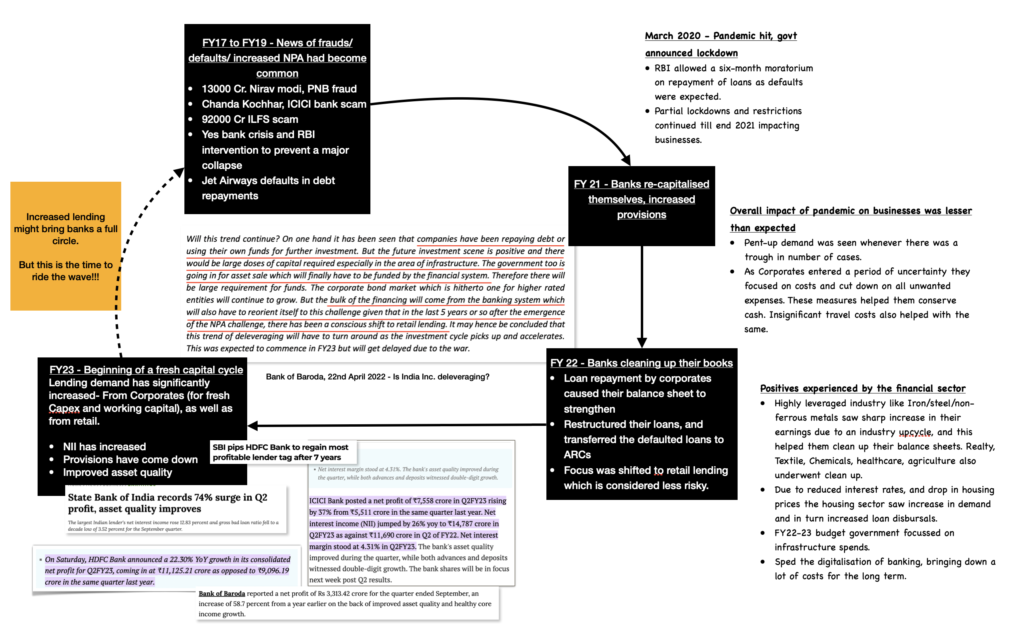

Banking cycle and it's impact on portfolio companies

Having observed a few events in the past couple of years has helped me understand the banking cycle better. This is how the past 5 years of the industry added up to my understanding.

Source: A Rough Book

The gist is we are entering a fresh capital cycle now..

Question is how to use this information to our advantage?!

I have decided to play this cycle with ICICI and IDFC First Bank.Started rebuilding position on ICICI bank after I saw a twitter thread on how their growth has been surpassing HDFC Bank y-o-y every quarter, the timing also seemed good, as the stock had been moving sideways at the time. Have been tracking few of their parameters over 2 years, and they have sustained their improvement.The position in IDFC first bank, will be a learning on how a bank franchise can grow and what are the variables to watch out for.

Current investments

Kotak Bank – Minor holding, not adding

HDFC Bank – Minor holding, not adding

SBI – Have been booking profits (cost price down to Rs.82). Currently, SBI is having good asset quality, growth in loan book; which must translate to higher profitability. Will take this opportunity to book profits again and make the stock zero cost.

ICICI Bank – Started investing in 2018, sold some in 2019, and made fresh additions from Dec 2021 onwards. Currently it is 8% of the portfolio, will not be making fresh investments further.

IDFC First Bank – Still building position

Tracking ICICI Bank

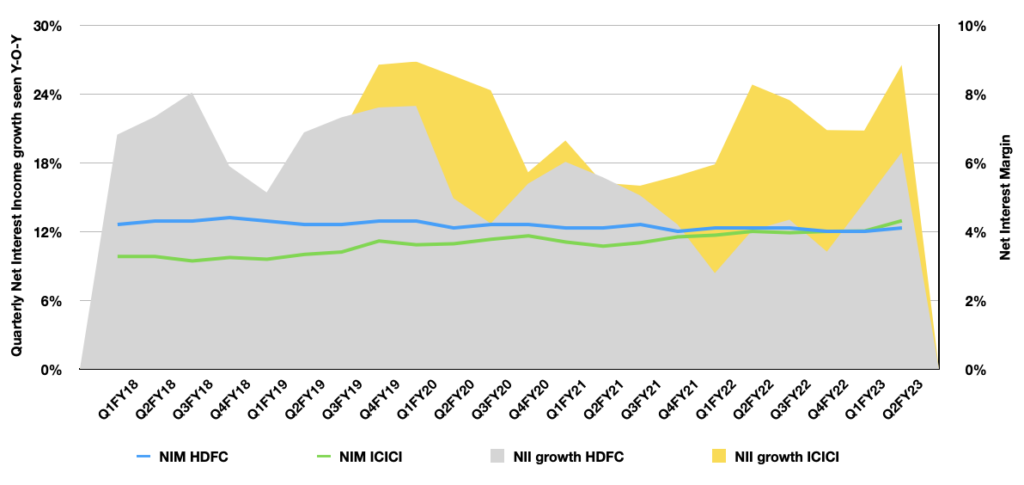

Building data on ICICI bank in order to track better and will keep HDFC Bank as the benchmark to monitor, due to it’s impeccable track record.

While HDFC Bank has been very consistent in all parameters, ICICI bank has shown significant improvement over the years.

Sandeep Bakshi joined ICICI in October 2018 when Chanda Kochhar resigned, since then the banks transformation is visible through improvingasset quality, growth rate and returns. They have consistently beaten HDFC Bank Y-O-Y in Net interest growth for past 15 quarters.

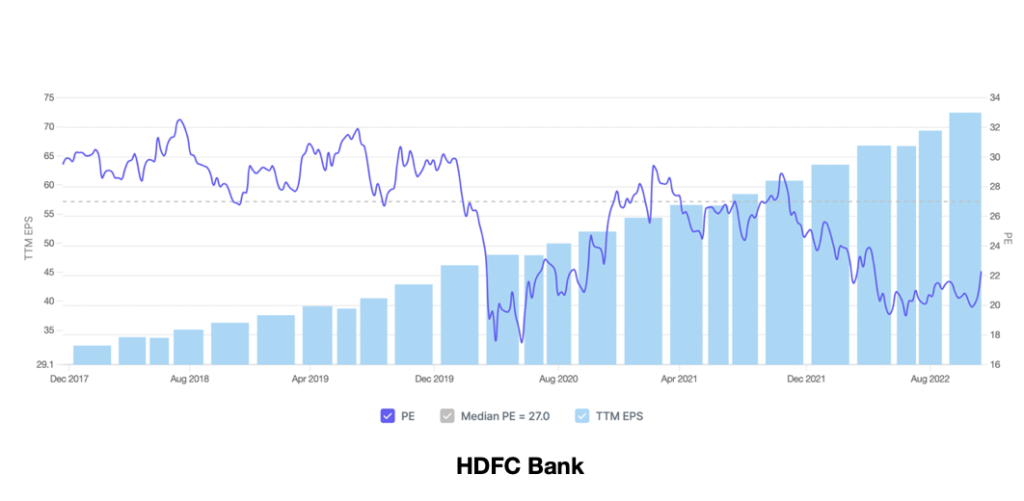

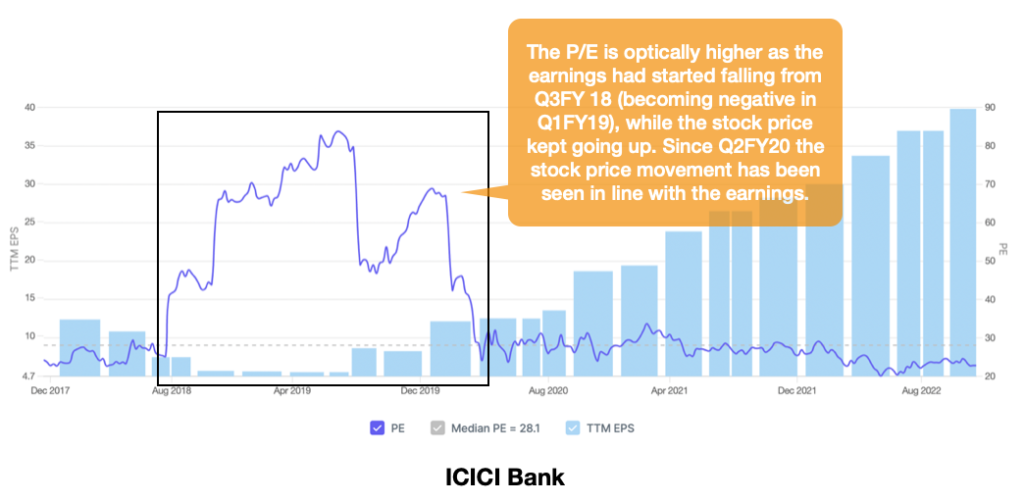

Valuation – Both trading slightly below their mean P/E; with similar P/S and P/B. HDFC does deserve a slightly better multiple than ICICI due to it’s flawless past perfomance.

Things I would watch out for –

Current CEO Sandeep Bakshi has been elected for another term (till 2026) which is positive, but will track any other significant changes in managment. Corporate governance issues have happened in the bank once, and hence is something to be careful about. I believe that problems could not have been limited to Chanda Kochhar.

According to a recent mint report retail loan book has been seeing increased slippages due to aggressive lending. The high risk products like credit cards and unsecured personal loans within retail, needs to be tracked.

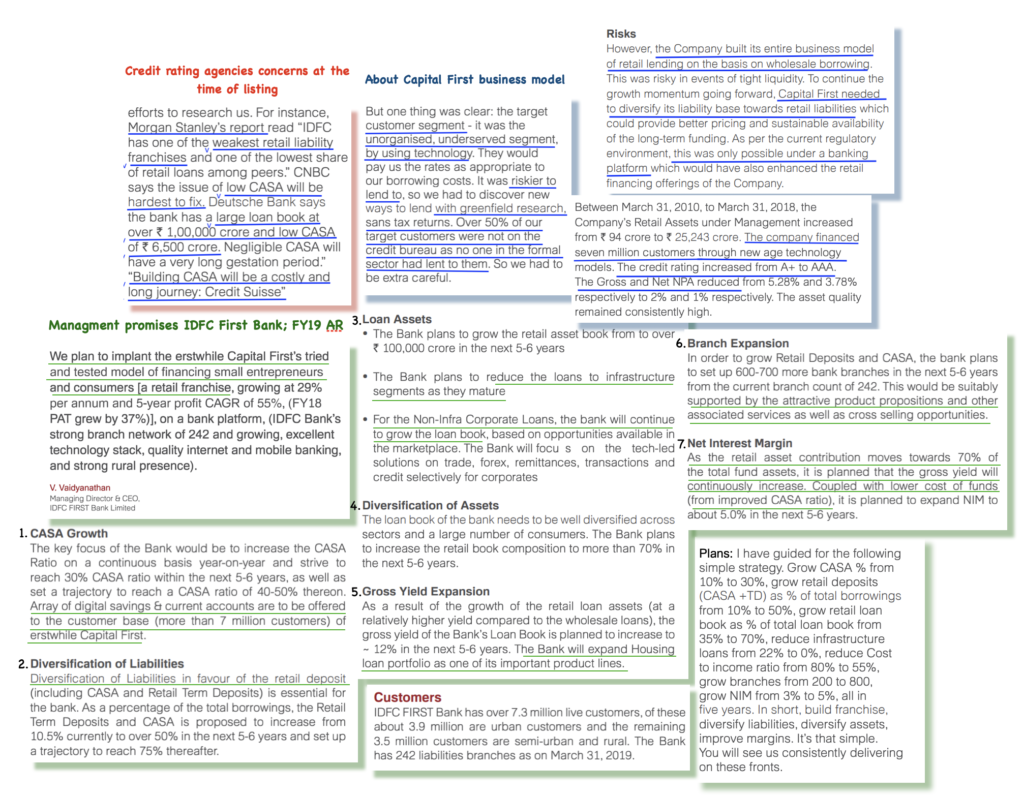

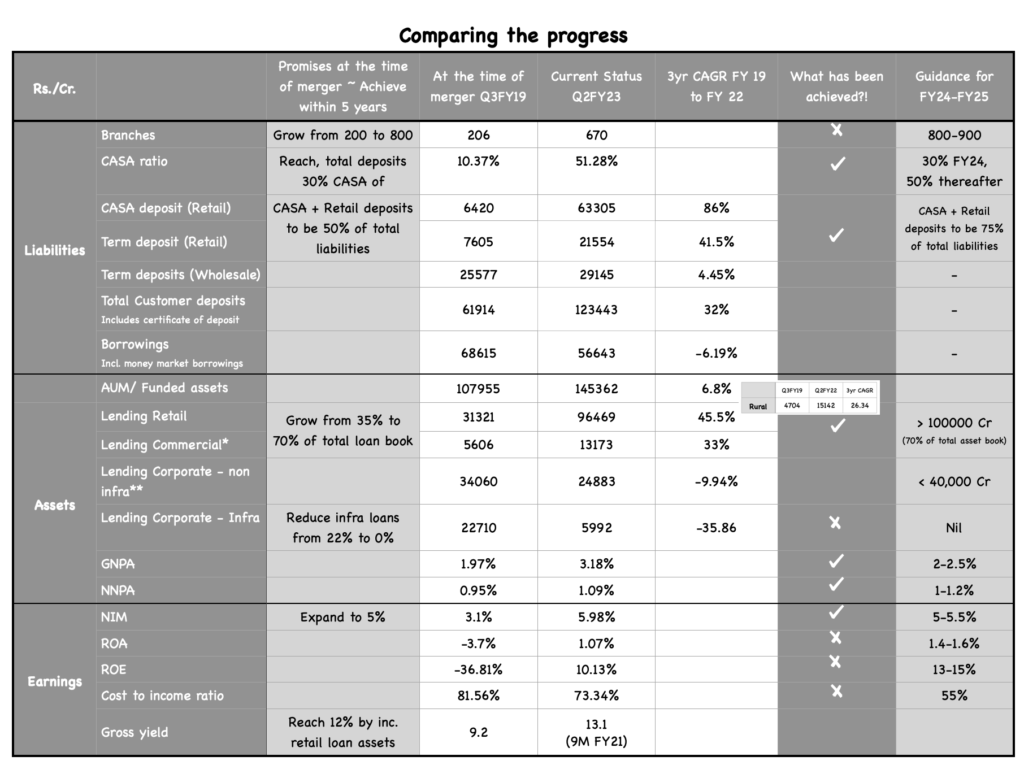

IDFC First Bank - Has the managment ‘Walked the Talk’

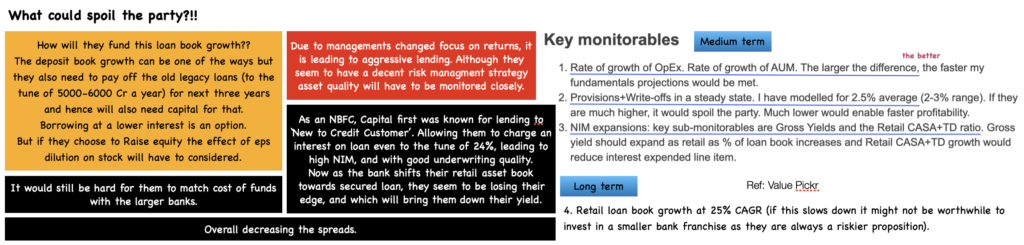

The gestation period of the bank is over. They are at a stage where earnings should start showing up as the major costs related to operations have been incurred and seems like all the surprises in asset quality have been factored in. The bank currently is available at a P/B lower than the larger ones; but if they succeed to bring in steady profit growth (while achieving return ratios) and 25% retail loan book growth (while keeping the asset quality stable), there should be no reason why a stock rerating will not happen.

After reading IDFC First Bank it occurs to me like a story having a past, a present and with a future (where a whole lot of retail investors are waiting to see how it unfolds).. I am feeling very passionate about this, as it has taught me many things about the banking sector.

Past…

The merger of IDFC Bank and Capital first took place in Dec 2018.

IDFC Bank started its operation as a bank (in 2015) after demerger from IDFC Ltd, a domestic infrastructure financing Institution in 1997. The loan assets and borrowings of IDFC limited were transferred to IDFC Bank at inception; and hence when when Idfc first bank merger took place it had some legacy issues of stressed corporate book and high infrastructure loans.

Capital First was a consumer and MSME financing entity since 2012 with a track record of decent growth, profits and asset quality.

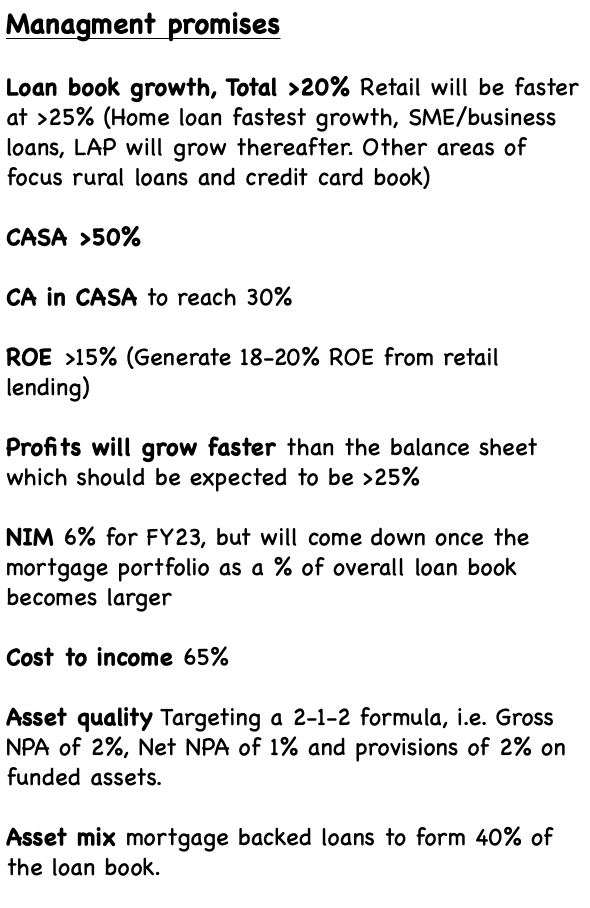

The managment’s major promise was turning the bank into a strong retail franchise, with diversified retail asset book.

But the skeletons in the IDBI banks lending books comes to haunt them in the form of DHFL, Reliance Capital and Vodafone-Idea. At the time of merger the stressed asset books were provisioned for so it seemed that IDFC first would start with a clean book with no asset troubles. But IDFC Bank was no outlier and faced the troubles which came when the economy went through a bad loan cycle. Constant provisioning and write offs taken affected their profitability. To make things worst covid happened, which was not factored into the growth plan. This had a major impact on profitability and return ratios.

Source: A Rough Book

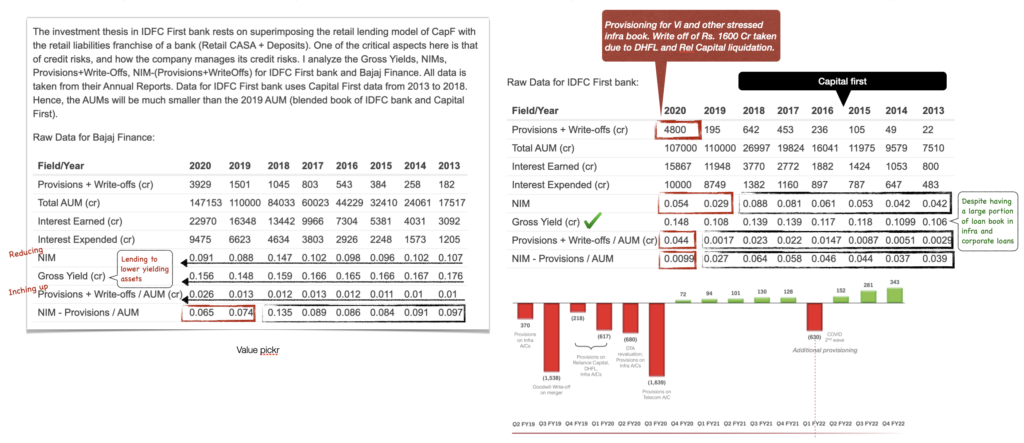

Because we are looking at a retail focussed Bank, comparison with Bajaj finance will help get a status quo on the possibilities of a retail franchise, which the bank is trying to build.

At the same time, Capital first helped them stay on their goal. Having started with a decent size retail customer base (3.5 mn) they had good cross-selling opportunities. The bank aggressively built on their asset book by giving deposit rates highest amongst peers and hence achieved a CASA of close to 50% in no time. The total customers have reached to 6mn+ now.

Due to an increase in deposit book of the bank there were some positive trends seen in the yield and cost of funds, leading to better spreads.

If we benchmark it against ICICI (yield of 7.4), their total yields are much higher at 13%. They are more in line with Bajaj finance (yield of 15.6%). Now that is a sweet spot to be in, having yields of an NBFC and the cost of funds of a bank. Will keep a keen eye on how that moves from here on. And ofcourse because of this their NIM now is higher than ICICI and HDFC Banks.

Future...

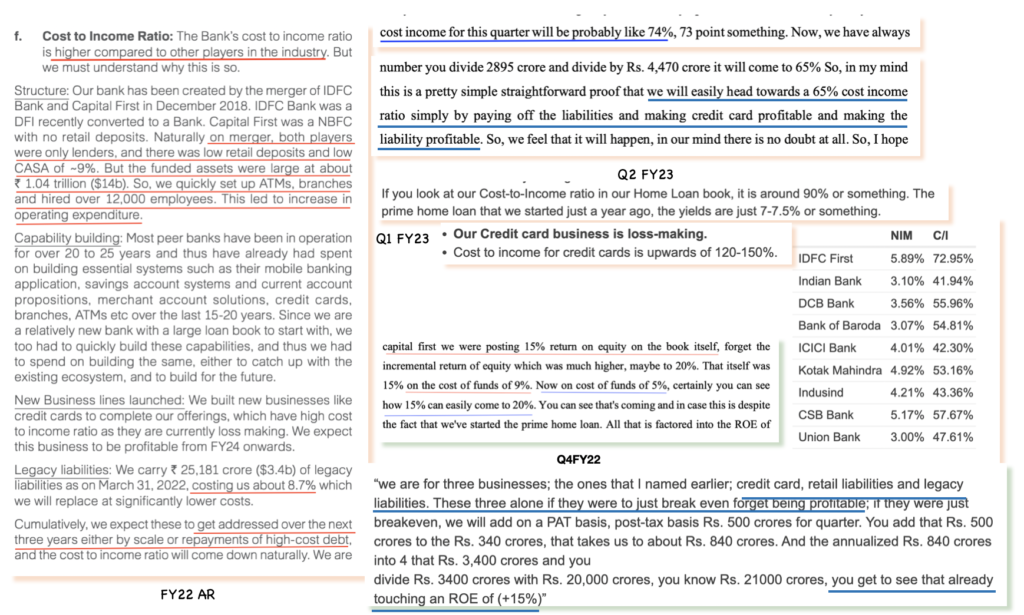

The bank has a Net Interest Margin which is amongst highest in the industry, but their Cost to Income ratio is also the highest. These higher costs were due to investments made in growing branches, atm, capital expenditure in digitalisation and growing newer verticals like credit card, home loan segment etc.

In order to strengthen their liability book there was a hold back on loan book growth for three years. Now that has happened, there is also an expectation to keep growing it at a decent pace and the asset quality issues have also stabilised; they are changing their focus towards loan book growth and right asset mix.

Once the AUM starts growing, expectation is majority of the the costs were front ended and will be divided with a larger base, reflecting into higher profitability.

So decreasing cost to income ratios, sustainable profitability and improving returns is the managements new tell.

Current institutional holding in bank is low, with high free float. Plus, the stock is trading at a P/B of 1.6, much below the P/B of 4.0 which the larger banks trade at. And hence a sustainable earnings upgrade could be followed by stock re-rating..

This is the happy ending we are all looking for.

16th March 23

Consequences of Asset - Liability Mismatch

While I was studying IDFC First Bank, I remember a friend mention, ‘it all now depends on how they strengthen their liability book’. I could not completely understand that statement then. But the recent ‘Silicon Valley Bank’ fallout has had a few learnings.

Think through more deeply of the sources of fund in a bank and usage of those funds, rather than just tracking the usual parameters like NII, NIM, ROE and asset quality.

Within a banks liability book, their bond maturity, it’s term and their interest rates also have to be monitored as closely as the advances made and their quality.

As these bonds could be locked in for longer tenures, interest rates hike can cause their value to decrease faster during that time. If pre-matured with-drawl is to be taken, then apart from penalty, bond yields should also be considered. High interest rates leads to lower bond yields as the spread tends to decrease.

Time value of long duration bonds is an important consideration to be made.

2nd May 23

Another impact of interest rate hike ~ Conversion of CASA into term deposits

While H2FY23 results of banks looked very good, with NIM at an all time high. What was already understood is that the NIM would not sustain as the banks had taken rate hikes on lending while not passing them on to depositors, but the higher interest rate on deposits have brought forward a new challenge for banks.

It has led to account holders parking their money into term deposits rather than leaving ideal cash in their account.CASA is the cheapest form of capital for any bank and if that CASA shifts to deposits, their cost of capital increases.

An uptick in loan growth against deposits (1.7x for SBI, need to check for others), will lead to banks having borrow from RBI at a higher repo rate affecting their NIM largely.

The Ken - 21st March 2023

CASA was not only interest free, it also helped generate other income in form of fees on those accounts. Hence, it should be tracked which banks have the highest reduction in CASA and what are they doing to gain it back.

2nd May 23

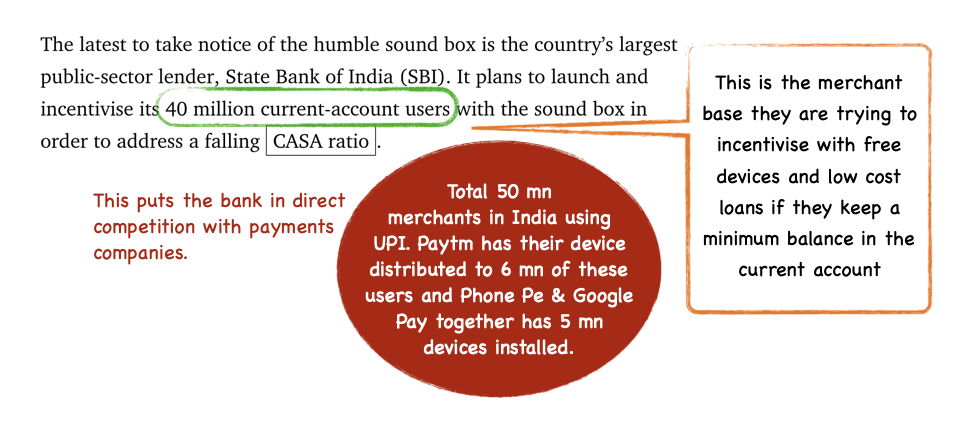

This way they enter into the payment company’s space. Up until now both seemed to have been collaborating, rather than directly competing with each other. Would this increase the cash burn for payment companies again, or are they already entering the matured phase of distribution cycle that the banks will have to work really hard to make any dent into their market share?!

Any success weakens the merchant base for Paytm, which was their largest strength and most important piece for lending business to succeed.

5th Sep 23

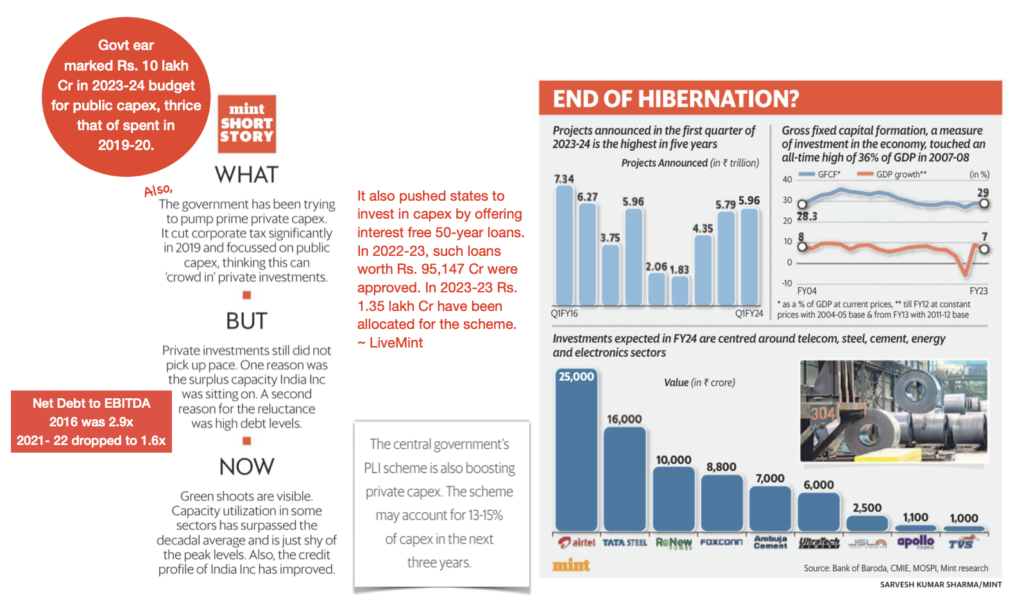

Return of Corporate lending

India Inc is finally increasing their capex. Gross fixed capital formation (GFCF) a measure of investment in economy peaked at 36% of GDP in 2007-2008, has finally been seen increasing.

This is a positive for banks as corporate advances would finally come back.

5th Oct 23

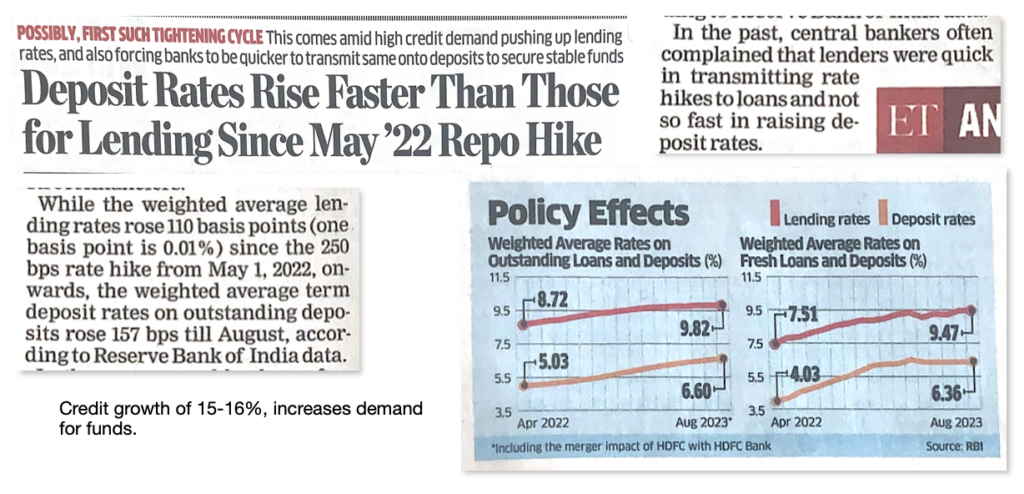

Pressure on NIM

In the current credit cycle, banks are raising funds by giving deposit at higher rates, while the increase in lending rates remain lower.

This lag of pass through in advances has to show up as lower margins.