17/10/22

Took out gains from Tata Elxsi on 12/08/22 as the P/E crossed 100x and I felt it was getting over heated. This reduced the cost price of stock to Rs. 21.

Average buying price was Rs. 1150.

Selling price Rs. 10150, making it one of my best returns.

In hindsight, it was a great decision as the stock peaked at 10,238 and has been on a downward trend since. Today the price fell 8% as the quarter results were a little slow, but not bad. This was my fear when I took the decision to sell, that a little slow down in earnings or margins can show a magnified effect downwards in price.

Analysing the decision

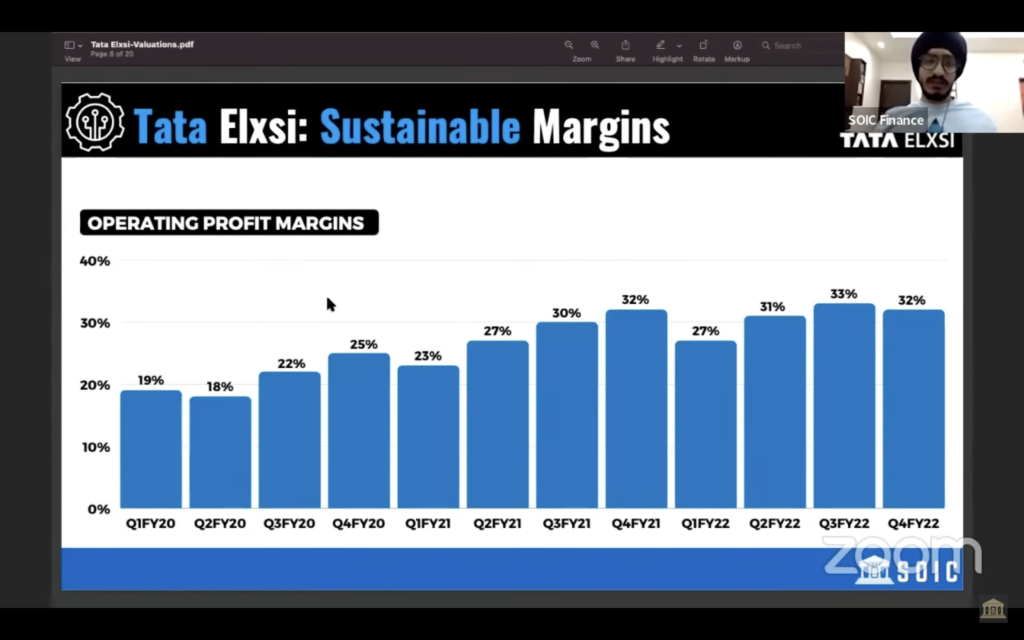

EBITA expansion had caused the P/E to expand, leading to the stock becoming a multi bagger. Now if that does not sustain and it again starts to trade at it’s average P/E of 30-35x, the market cap can even halve from current levels.

I still believe in the business (also a bit biased as it is an innovation led, speciality business), and would like to remain invested in it for the long term.

But a question that occurs to me is –

‘Under such circumstances is it better to take out gains and zero the cost; or to exit the stock completely?!’

Would I consider buying again into the business?

Yes, if it starts consolidating again at 50% from peak for 6 months.

Taking a relook today it occurs to me that the company still trades at a premium to other ER&D players and hence the stock price might go into time correction. If the price stays stable around 65oo and the revenue shows growth with stable margins, would consider adding back again.