@ Market Cap of Rs. 12700 Cr, CMP 798

My first purchase was in June’24 (Market cap of Rs. 9000 Cr), and have averaged since then. Started tracking in Sep’23 when the new CEO joined, but the business at the time was taking a hit on it’s revenue and profitability in all segments.

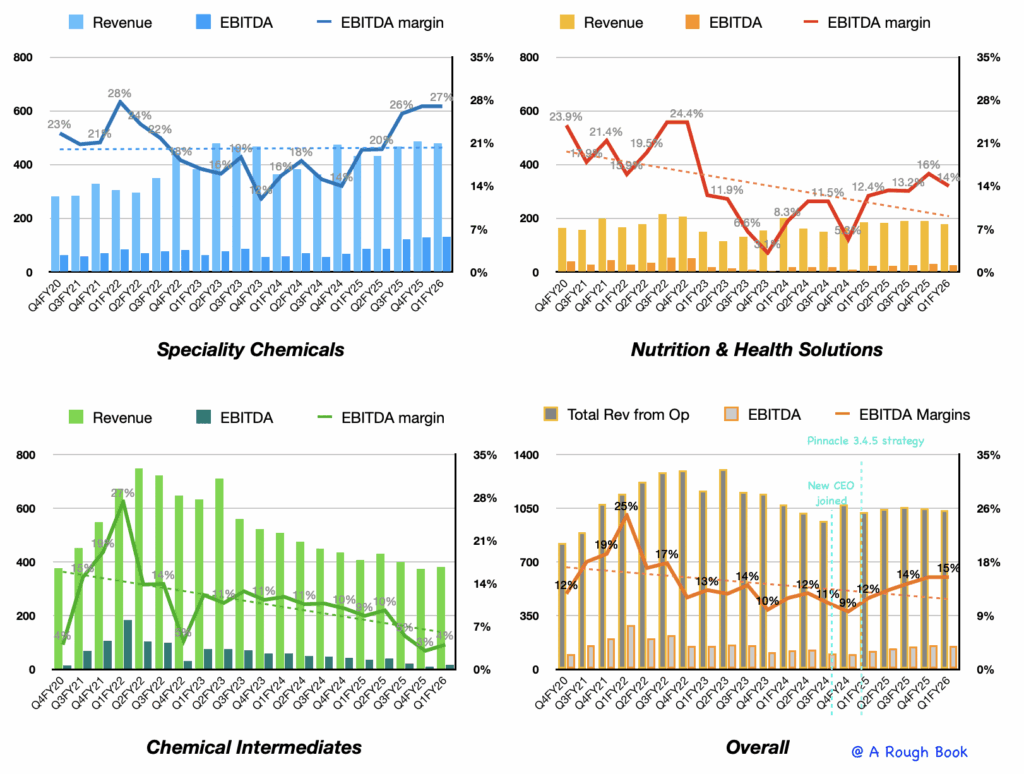

- Chemical intermediates which was the highest contributor to their revenue, was coming off a high base post covid. Acetic anhydride an important bulk chemical for the company is used in paracetamol; their volumes took a hit, while affecting the spreads.

- The broader agrochemical industry was impacted due to channel de-stocking and dumping from China. Chemical Int revenue was affected due to this as well because high volumes of acetic anhydride went into agrochemicals end use. While, agrochemicals also contributed 1/3rd to their specchem revenue.

- Within Nutrition segment Niacinamide prices saw pressure due to increased competition from Chinese players..

Reversion in Revenues and Profitability as Business Mix Turns towards Speciality

This can be observed in the below graphs, along with bottoming out and business mix change.

There is a transformation happening in the business and which is reflecting in it’s numbers.

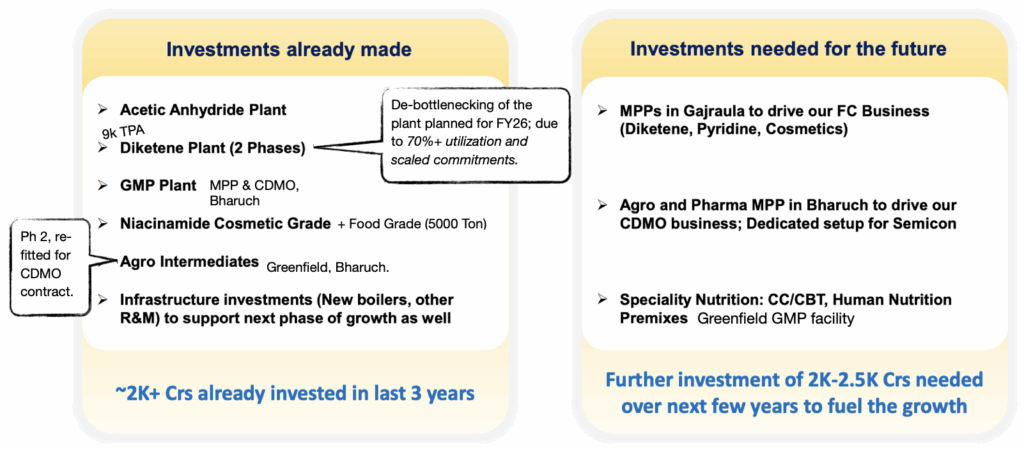

They had announced a capex of Rs. 2000 Cr in FY22 (w revenue base of Rs. 5000 Cr). Company remained optimistic about future opportunities and continued with their growth capex even when they faced headwinds in FY24 and FY25. The revenue has still not crossed the FY22 base and another fresh capex of Rs. 2000 – 2500 Cr has been announced in FY26.

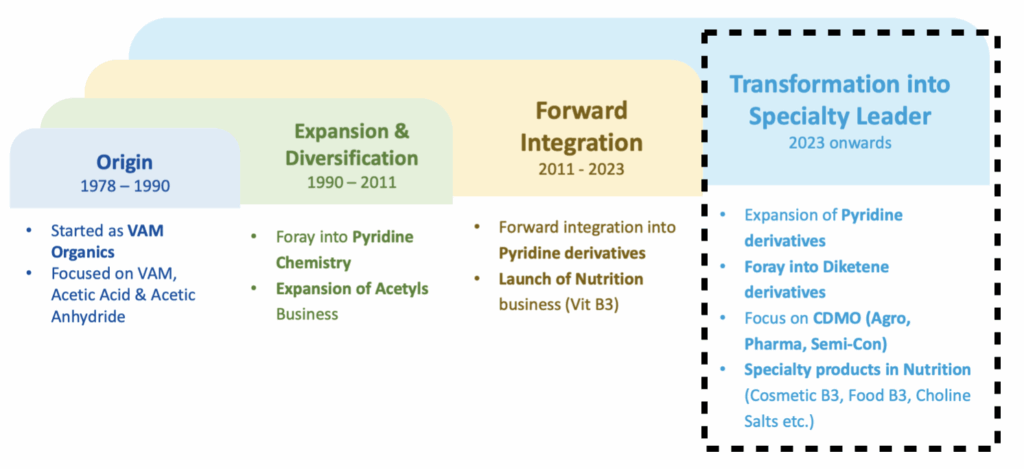

Pyridine-Picoline and Acetic anhydride/Ketene are two parallel chemistry platform for Jubilant Ingrevia. They complement each other by serving similar end-markets of pharma and agro businesses — which is why they are synergistic in terms of customer base and R&D.

Under the new strategy Ingrevia is leveraging their legacy chemistry skills and forward integrating. Thus they move up the value chain into high-value products (specialty and fine chemicals), and towards end-use markets which are more stable.

- Ingrevia started as a Pyridine (intermediate) supplier to global agrochemical and pharmaceutical companies. Later, forward and backward integrated, having products within the value chain of all three business segments. Being present across the value chain gives them cost advantage, and thus are ‘Globally lowest cost producer’.

- Mid 2000s moved downstream into value-added products like Beta Picoline used in Niacin / Niacinamide (Vitamin B3) (part of their Nutritional segment) and other Pyridine derivatives (part of the spec chem business).

- Leveraging their strong base in acetyl and captive ketene production forward-integrated into Diketene chemistry. Diketene and its derivatives have higher value and diversified end-use markets compared to bulk acetic anhydride. Currently have 6 products, 4 will be launched this year.

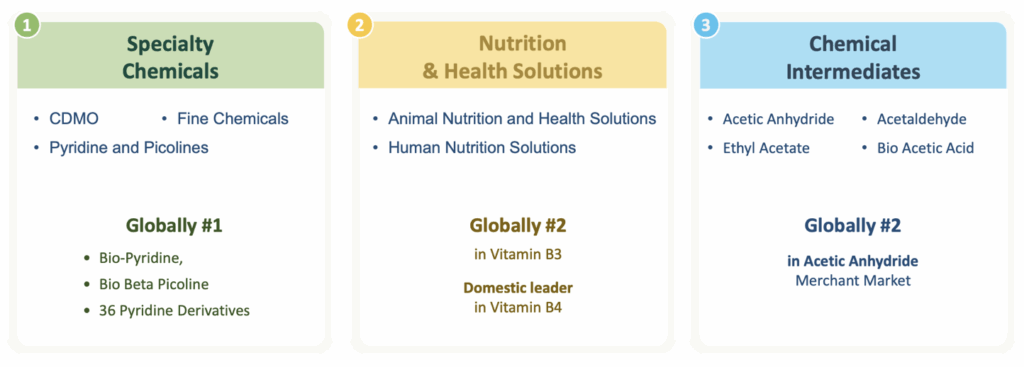

3 Business verticals: Speciality Chemicals, Nutrition & Health solution and Chemical Intermediates

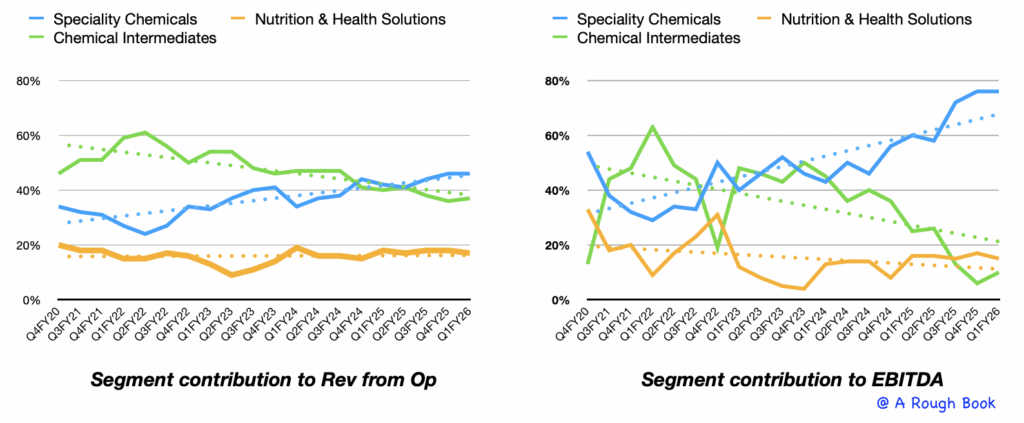

Chemical Intermediates used to make 50% of product mix, which is changing. By doing value addition within the Speciality Chemicals and Nutrition segment.

- Speciality Chemicals

- Within Pyridine and Picoline, focusing to enter newer end use segments like oil fields (low vol, high value). Could be focusing to fill in the gap left by Vertellus oilfield portfolio category.

- Pyridine and Picoline derivatives (fine chemicals) are constantly being expanded through the years. 52% of these are used captively in value added Speciality chemical products or in nutrition. Cosmetic/Microbial solutions business is at scale up stage.

- Diketene (fine chemical) production has started, which is a higher margin product.

- CDMO focus is on agro, pharmaceuticals and semi-conductors.

The company has signed two agrochemical contracts for September and October 2024, including a significant $300 million deal with Innovator 2. Additionally, it is in advanced discussions for 3–4 more contracts.

Currently they are 9 molecules under development in Pharma.

- Pyridine and Picoline also has an application in semiconductors, electronics etc. Company has initiated focus on dedicated Semiconductor team with required infrastructure (lab and pilot plants). 8 molecules are under development- E-pyridine and E-choline.

2. Nutrition and Health

- Jubilant Ingrevia is moving from animal grade to cosmetic and food grade Niacinamide, which has higher margins. USFDA approval received for their GMP facility. This plant will allow the company to enter the global infant nutrition market with food-grade Niacin.

- Choline Salts (Choline Chloride and Choline Bitartrate (Vit B4) is another anchor products for food segment. GMP Greenfield facility being planned.

- Plan is to Foray into Premix / other vitamins within both these, they already have animal nutrition pre-mixes portfolio in India and neighbouring markets.

Currently human nutrition (cosmetic and food) make 31% of the total Nutrition portfolio, and guidance is to take it to 67% by FY30. – Q3FY25

3. Chemical Intermediates

- Acetic anhydride is the main revenue driver, it’s demand remains low currently due to softened end market of paracetamol, however they have managed to hold onto their market share.

- Ethyl acetate another important intermediate sold in merchant market.

45% of these intermediates like ethanol, acetaldehyde and formaldehyde are consumed captively.

Ambition released in Feb 2024

All the initiatives have been aligned for the same.

- Capex of Rs. 2050 Cr done between FY22 – FY25. Another Rs. 2000- Rs. 2500 Cr announced for the next 4 years.

- Business mix shift towards speciality.

- Lean structures are being adopted through multiple efficiency initiatives focused on yield and energy cost optimisation, overheads reduction exercise etc. Leading to FY25 savings of Rs. 120 Cr, the benefits of which are going to flow into the entire Pyridine value chain. Lean 2.0 launched with Rs. 100 Cr+ savings target.

- Constant focus on working capital management, converting almost 100% operating profits to operating cash. Net working capital to turnover was 17% in Q4FY25 against 22% Q2Y24. Working capital days reduced to 67 from 89. Because of which they have been able to manage their capex with minimum debt, even during the business down cycle.

- Roadshows across EU/US/Japan; 120+ customer meetings.

- 40+ focused projects in R&D pipeline with expanded team to 150+ scientists (26 PhDs).

- Streamlining of top org structure to bring more agility.

Based on Guidance

- From initial Rs. 2050 Cr Capex, Rs. 9500 Cr revenue expected by FY27. And incremental Rs. 2000 Cr Capex at 20% ROCE, should be able to give another Rs. 3000 Cr revenue.

Spec chem when becomes more than 60% of the business, should give margins of 24% in steady state. Spec Chem business is already reaching 22% EBITDA margin in 9M FY25.

Reaching consolidated EBITDA margin in excess of 20% is possible.

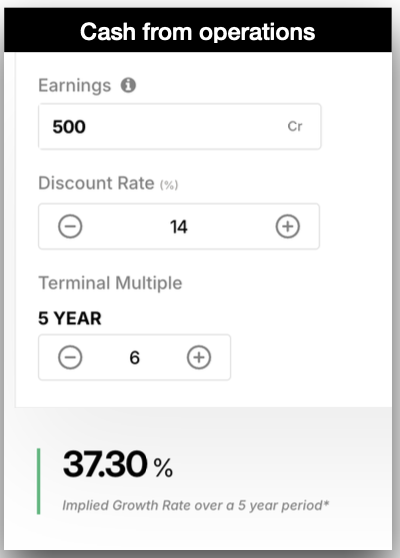

Combining the consolidated and Spec chem guidance, it seems there is a possibility of EBITDA to grow in excess of 5x as well. With continued focus on operations, the company may be able to give Rs. 1500 – Rs. 2000 Cr in CFO annually in 3-4 years.

Valuation

My base case (from the current price) is the stock will double in 4 years with consistent performance and slight re-rating.

My bull case would rest on the CEOs execution prowess.

Why I got interested in the business post the CEO joined??

The transformation in business is evident post his joining.

The business comes with a growth and stock re-rating potential.

Avg price of Rs. 650, 3% of portfolio