Initial analysis of the business said it is at the bottom of the earnings cycle due to impact of covid on the industry at large, once the business resumes to pre-covid levels upside would naturally come to the stock.

Why should I buy Thomas cook??! - 11/10/22

@ Today’s stock price of Rs. 78 (Market cap of Rs. 3680) – available at Pre – covid P/S of 0.54 x (Considering pre – covid sales of Rs. 6800 as the base).

Median P/S of the company has been 0.5x in past 5 years, so any earnings re-rating should have positive impact on stock rerating.

Once it reaches this stage there can be two actionable – Profit booking/ Hold

Hold if they are able to exceed profits beyond Rs. 90 Cr @ Rs. 6800 Cr. of sales.

Why??? Because that means there is margin expansion and there is possibility of stock re-rating beyond 0.5x P/S..

What could work in their favour for margin expansion?

Sterling hotels have turned EBITDA positive post covid (with 20-25% margins) and Digiphoto servicing also turned EBITDA +ve last quarter.

Lot of cost cutting measures were taken during covid and digitalisation efforts were made. 30-35% reduction in cost was achieved, and the managment has indicated that it is to stay..

What could work in their favour for stock re-rating?

FII and DII holding in the company is at 5 year low.

Why should I not buy Thomas cook??! - 11/10/22

Tracking parameters

- Growth in the travel industry

- Revenue mix shift

- Acquisitions by the company

- Operating profit to operating cash conversion, FCF generated

Industry Takeaways

- Domestic business has been very strong

- Travel related spends are expected to increase, with increasing middle class in our country

- The good businesses, inorder to sale covid went through major cost cutting, which they think are here to stay

- There is a demand-supply gap, favouring the hotel industry currently, their Average Revenue per Room have gone up considerably

Bought at avg price of Rs. 77, investment @ 2.92% of total portfolio

Why should I add Thomas cook??! - 28/02/23

@ Current Market cap Rs. 2900 Cr (fallen majorly post the TCS announcement), stock is available at Pre-covid P/S of 0.42x (keeping the same pre-covid sales assumption of Rs. 6800 Cr)

On the positive side company has reported an EPS of 0.02 and 0.39 in Sep and Dec 23 quarters, against reported negative EPS in the prior 10 quarters.

Why should I not add?! - 28/02/23

Announcement of 20% TCS on overseas remittance by the government in recent budget, puts their outbound business at risk of returning back to normalcy.

Being a business with very low margins, the operating deleverage can make the PAT slip back to negative returns.

Added at Rs. 70, increasing investment to 4.28 % of portfolio

Why should I add Thomas cook??! - 12/08/23

- Next two quarters earnings visibility high as inbound travels primarily happen in Q3 and Q4 and overall bookings are positive.

- Expenses have come down 30% from pre-covid times and expected to sustain

- Travel business realisations has also got better; with volumes still at 78% of pre-covid level, profitability has already reached pre-covid. Further recovery will all flow to the bottom line. Expected expansion of margins is 7-8% from 3% once inbound and DMS business picks up.

- Digitalisation of various business segment increased productivity and reduced costs.

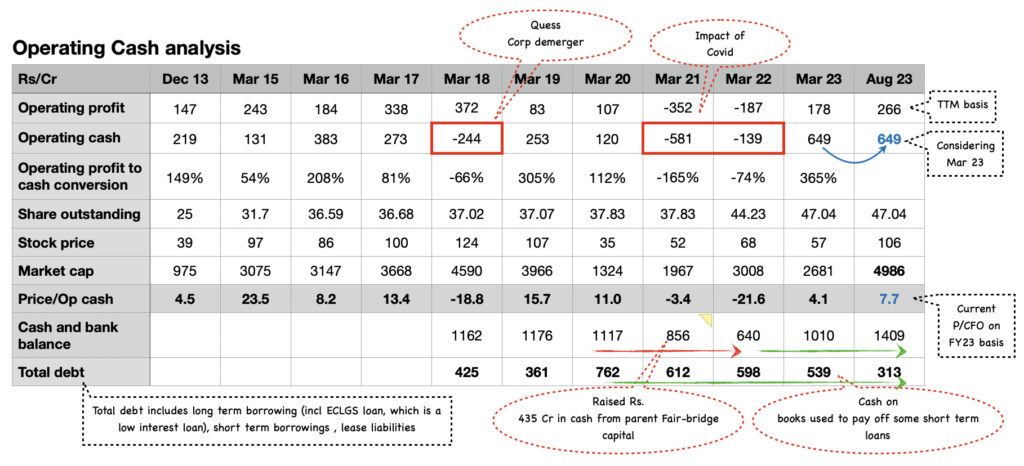

4. Balance sheet is healthy with total equity increasing due to retained earnings, debt decreasing. Current asset expansion comes from increase in cash on books.

5. Strong cash generating business model with high EBITDA to CFO conversion and negative working capital days.

- Receive advances from customer towards leisure tour/holiday’s packages, recognised only on the date of departure and arrival of the tour.

- Sterling hotel membership program

- Pre-paid forex cards develop positive float for the business

- Most business acquired through m&A are maturing – Sterling earned FCF of Rs. 100 Cr in FY23

Since Fairfax acquired Thomas Cook India in 2012, they have grown the business through various M&A (eg SOTC, Sterling, DEI etc). Although the managment is not indicating any acquisition plans for near future, I believe the ready cash will be of use if any opportunity comes by.

The impact of TCS would come on business post September 23, but post the clarification of 5% limit for remittance upto Rs.7 lakh per person per year, it is expected to be less than earlier assumptions.

Why should I not add Thomas cook??! - 12/08/23

@ Current Market cap Rs. 5000 Cr

The stock has run up 38% in the past one month and reached Rs. 106 from Rs. 76 (which is close to my average buying price).

This sharp rise can attract profit booking from the markets as it is trading above it’s historical highs, unless the growth in EPS continue at the same rate.

At this stage I am unable to quantify the re-rating markets would be willing to give the stock and hence the least that can be assumed is stock will grow in line with it’s profits.

No action taken, investment increased to 5.89 % of portfolio due to recent run-up in stock price

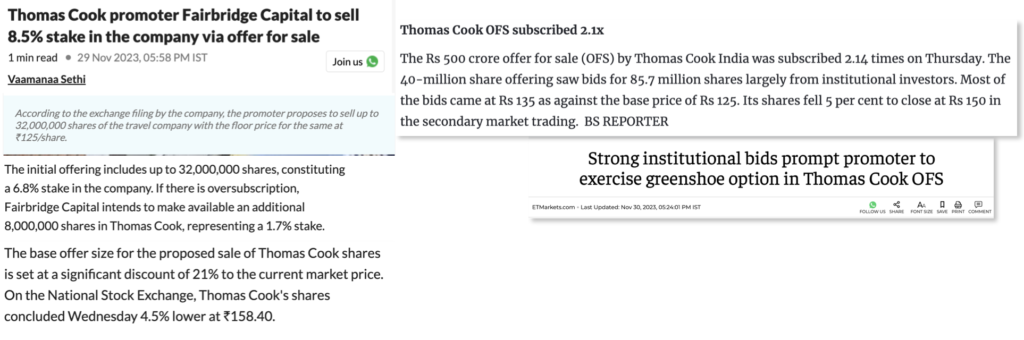

Promoters announce OFS - 01/12/23

@ Rs. 6782 Cr current market cap (this is post the 15% fall from it’s peak on 28th Nov 23 which came from the news, breaking the stocks strong momentum).

Sharp run up had happened post the Q2 results, where on a TTM basis the stock had reached FY 19 revenue. Stock started trading at a P/S above 1x..

This piece of news do not warrant any change in my stock position; but it still remains significant as both positive (OFS being subscribed at 2.1x ) and negative market sentiment were observed regarding the same.

I will make a fresh consideration if the stock starts trading below 20% of my benchmarked P/S of 1x ..

Why should I add Thomas cook?! - 19/03/24

@ Rs. 7136 Cr current market cap, the company has reached sales of Rs. 6900 Cr on Dec 23 TTM basis. The stock has seen a re-rating if TTM Dec 23 Sales are considered against Pre-covid sales of Rs 6800 Cr, as the profits have more than doubled from Rs. 90 Cr to Rs. 203 Cr (TTM Dec 23); thus reaching a P/S of 1x from FY 19 P/S of 0.54x.

The institutional investors who bidded in OFS have entered at an avg price of Rs.135 ie P/S Sep 23 TTM basis of 0.96x (with market cap of Rs. 6350 Cr and Sep 23 TTM revenue of Rs. 6591 Cr).. Although EV/FCF is a better matrix of valuing the company doing it with top-line numbers for finding an easy ball-park number.

OFS happened at EV/FCF valuation of 7x.. Not sure current value as FCF for Dec 23 is unknown at this stage.

There still seem value left in the business when compared with below data points –

1. Revenue and profitability growth triggers still present

- Travel business – Scope of margin improvement by 50-100 bps and revenue expansion coming from long haul improving.

- Strong order book to add to top-line – New contracts in DEI and Travel business (corporate B2B) to add 40 Cr and 200 Cr to top-line resp., according to Q3FY24 concall guidance from management.

- Sterling new key addition and occupancy being maintained at 60% – Focus now would be on improving RevPAR. Total number of rooms reached 2617 and 900 incremental rooms in the pipeline.

- More importantly travel sector continues to have tailwinds.

3. Further improvement in FCF generation coming from

- Float in financial services business increases as card penetration and loading increases

- Growth in outbound business which has negative working capital requirements

- Previous acquisitions mature and they become self sustainable

- Re-investments requirement to grow the business becomes lower due to shift in digital for travel and travel related business (thus less physical stores required for growth and digital infra cost largely factored in) and adoption of asset-light business model in Sterling

4. Sterling value if compared to other hotel businesses..

With demand exceeding supply the hotel business enjoys high valuation currently.. Based on that if we value the Sterling business it comes close to Rs. 3500 Cr (by giving them a 8x P/S and FY 25E revenue of Rs. 440 Cr) ie 50% value of full business/ atleast 25% if 50% holding company discount is considered.

9M EBITDA margin at 37% of Sterling is in line with the below hotel chains, so comparing the valuation with them is not far fetched..

P/S – IHCL @ 12x, EIH @ 11x, Juniper hotels @ 15x, Lemon tree @ 10x

Why should I not add Thomas cook?! - 19/03/23

@ Rs. 7136 Cr current market cap

Thesis of initial investment was recovery in sales to pre-covid and re-rating due to margin expansion.

Now the business has exceeded pre covid sales of Rs. 6800 Cr with recovery in all businesses other than long haul. The stock has also re-rated from it’s historical average, with improvement in business fundamentally and margin expansion.

P/S of 1x from avg of 0.5x. Op margin of the business has reached 5% (Dec 23 TTM) from 1% pre-covid, on Rs. 6800/6900 Cr of sale base.

P/FCF Dec23 TTM basis has reached 7x considering free cash flow in line with Sep 23.. While when the position was built in FY 23 the P/FCF was at 4.4x.

Institutional investors have just started entering into the business post OFS. Continued improvement in business and with tailwinds in the industry larger allocation from these set of investors may be expected.

Added at Rs. 150, increasing investment to 7.7 % of portfolio

From Value buy, analysing the business for long term growth potential… 7th Aug 2025

@ Rs. 7087 Cr current market cap

The stock seems to be stagnant for 17 months now. But in-between it also saw a high, reaching a market cap of Rs. 12,000 Cr.

Why am I still holding Thomas Cook?

Fairfax is known to create shareholder value. Till now the playbook has been to increase the intrinsic value of business through acquisition; incubate businesses under the travel segment and de-merge of non-core business at a higher valuation (eg Quess). Sterling seems to be one such opportunity which holds the potential of getting listed separately. While, the Rs. 400 Cr cash (other than the free float), gives them acquisition potential.

Post acquisition of Thomas Cook by Fairfax, equity dilution was carried out multiple times to fund the acquisitions (as well as covid). But now consolidated business has started showing ROE upwards of 15% and cash on books; showcasing prudence in capital allocation. (Meets Fair fax hurdle rate of 12-15% IRR expectation).

Valuation comfort

If the consolidated business is considered on a P/E basis, earnings are normalised and trading at 28-30x. Considering a potential of 10-12% growth in revenue and margins to stay at current levels, PEG is coming to 2.5x.

A better way to look at the valuation is through SOTP.

Current Enterprise value of the business = Rs. 7087 Cr + Rs. 465 Cr (debt) – Rs. 400 Cr (cash) = Rs. 7150 Cr.

By breaking it down, and doing an SOTP valuation…

- Sterling – EBITDA Rs 171 Cr * 20x = EV of Rs. 3500..

IHCL EV/EBITDA is 35x, EIH @ 23x, Juniper hotels @ 32x, Lemon tree @ 21x

DEI – EBITDA Rs. 85 Cr * 6x = Rs. 500 Cr (Similar EV/EBITDA of 6.8x as paid during acquisition). Deal at Rs. 289 Cr in 2019, with FY 2018 sales of ≈Rs. 450 Cr and EBITDA of Rs 42.5 Cr, did FCF of Rs. 36 Cr.

Travel and related services – EBIT Rs. 249 Cr * 10 x = Rs. 2500 Cr

Cash generating business due to -ve working capital cycle.

Financial services – EBIT Rs. 150 Cr * 10 x = Rs. 1500 Cr. Pre paid card generates float for the segment.

…the total Enterprise Value comes to Rs. 8000 Cr. Which shows that the business is available at a discount of 14%.

Thomas Cook accounts for 2% of Fairfax’s overall portfolio and 20% of its India holdings. The key question is whether the business holds enough strategic significance for Fairfax to actively engage at the board level and drive further shareholder value creation.

Investment is down to 6.3 % of portfolio, stock price has come back to Rs. 150.

No action taken, as I find better opportunities to allocate capital within the portfolio. I would add if discount increases further and book profits if the stock reaches it’s previous highs.